- New Zealand

- /

- Electrical

- /

- NZSE:AOF

It's Down 29% But AoFrio Limited (NZSE:AOF) Could Be Riskier Than It Looks

The AoFrio Limited (NZSE:AOF) share price has fared very poorly over the last month, falling by a substantial 29%. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 51% loss during that time.

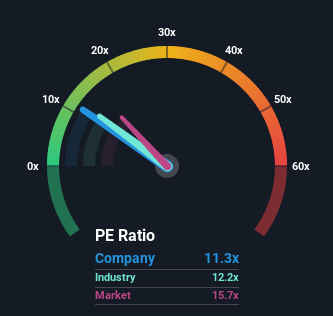

After such a large drop in price, AoFrio's price-to-earnings (or "P/E") ratio of 11.3x might make it look like a buy right now compared to the market in New Zealand, where around half of the companies have P/E ratios above 16x and even P/E's above 27x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

For instance, AoFrio's receding earnings in recent times would have to be some food for thought. It might be that many expect the disappointing earnings performance to continue or accelerate, which has repressed the P/E. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

See our latest analysis for AoFrio

Is There Any Growth For AoFrio?

The only time you'd be truly comfortable seeing a P/E as low as AoFrio's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a frustrating 40% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 349% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Comparing that to the market, which is only predicted to deliver 5.5% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

With this information, we find it odd that AoFrio is trading at a P/E lower than the market. It looks like most investors are not convinced the company can maintain its recent growth rates.

The Bottom Line On AoFrio's P/E

The softening of AoFrio's shares means its P/E is now sitting at a pretty low level. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of AoFrio revealed its three-year earnings trends aren't contributing to its P/E anywhere near as much as we would have predicted, given they look better than current market expectations. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

Having said that, be aware AoFrio is showing 3 warning signs in our investment analysis, and 1 of those shouldn't be ignored.

Of course, you might also be able to find a better stock than AoFrio. So you may wish to see this free collection of other companies that sit on P/E's below 20x and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:AOF

Flawless balance sheet and good value.

Market Insights

Community Narratives