Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Cloudberry Clean Energy AS (OB:CLOUD) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Cloudberry Clean Energy

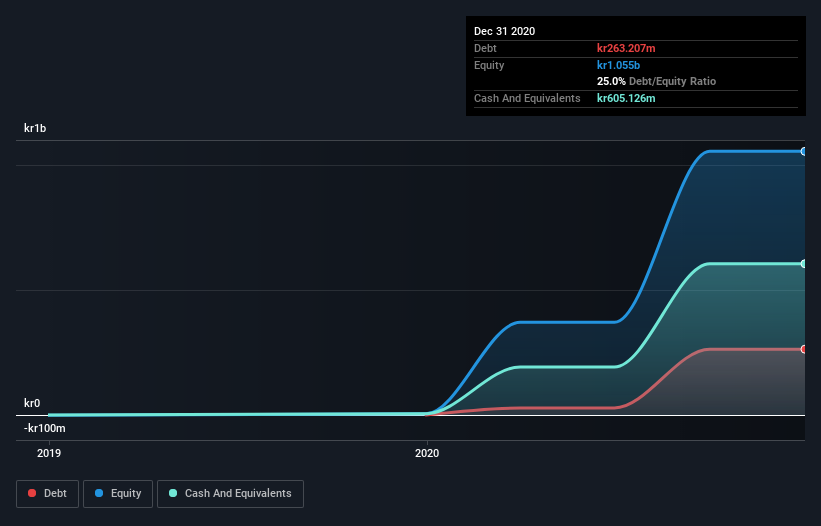

How Much Debt Does Cloudberry Clean Energy Carry?

The image below, which you can click on for greater detail, shows that at December 2020 Cloudberry Clean Energy had debt of kr263.2m, up from none in one year. However, it does have kr605.1m in cash offsetting this, leading to net cash of kr341.9m.

A Look At Cloudberry Clean Energy's Liabilities

Zooming in on the latest balance sheet data, we can see that Cloudberry Clean Energy had liabilities of kr282.9m due within 12 months and liabilities of kr59.3m due beyond that. On the other hand, it had cash of kr605.1m and kr2.83m worth of receivables due within a year. So it can boast kr265.8m more liquid assets than total liabilities.

This surplus suggests that Cloudberry Clean Energy is using debt in a way that is appears to be both safe and conservative. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Succinctly put, Cloudberry Clean Energy boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Cloudberry Clean Energy's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Cloudberry Clean Energy reported revenue of kr3.6m, which is a gain of 1,144%, although it did not report any earnings before interest and tax. That's virtually the hole-in-one of revenue growth!

So How Risky Is Cloudberry Clean Energy?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Cloudberry Clean Energy had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through kr7.2m of cash and made a loss of kr34m. However, it has net cash of kr341.9m, so it has a bit of time before it will need more capital. The good news for shareholders is that Cloudberry Clean Energy has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Cloudberry Clean Energy you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Cloudberry Clean Energy or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OB:CLOUD

Cloudberry Clean Energy

Operates as a renewable energy company in Norway, Denmark, Switzerland, and Sweden.

Reasonable growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor