- Norway

- /

- Marine and Shipping

- /

- OB:WAWI

Is Weakness In Wallenius Wilhelmsen ASA (OB:WAWI) Stock A Sign That The Market Could be Wrong Given Its Strong Financial Prospects?

Wallenius Wilhelmsen (OB:WAWI) has had a rough three months with its share price down 11%. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. Specifically, we decided to study Wallenius Wilhelmsen's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for Wallenius Wilhelmsen

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Wallenius Wilhelmsen is:

32% = US$1.1b ÷ US$3.3b (Based on the trailing twelve months to December 2024).

The 'return' is the yearly profit. Another way to think of that is that for every NOK1 worth of equity, the company was able to earn NOK0.32 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Wallenius Wilhelmsen's Earnings Growth And 32% ROE

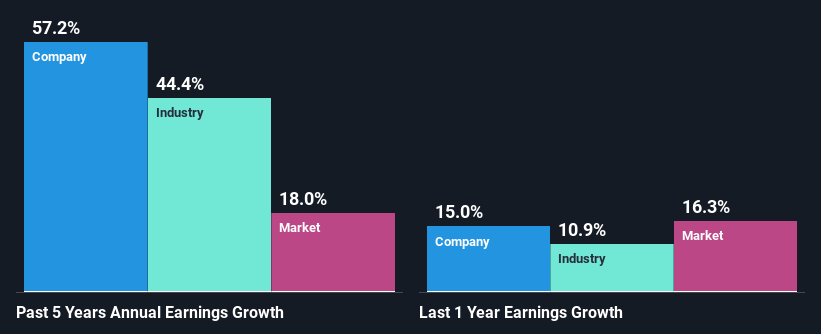

First thing first, we like that Wallenius Wilhelmsen has an impressive ROE. Additionally, a comparison with the average industry ROE of 30% also portrays the company's ROE in a good light. Therefore, it might not be wrong to say that the impressive five year 57% net income growth seen by Wallenius Wilhelmsen was probably achieved as a result of the high ROE.

Next, on comparing with the industry net income growth, we found that Wallenius Wilhelmsen's growth is quite high when compared to the industry average growth of 44% in the same period, which is great to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Wallenius Wilhelmsen is trading on a high P/E or a low P/E, relative to its industry.

Is Wallenius Wilhelmsen Making Efficient Use Of Its Profits?

Wallenius Wilhelmsen's significant three-year median payout ratio of 51% (where it is retaining only 49% of its income) suggests that the company has been able to achieve a high growth in earnings despite returning most of its income to shareholders.

Moreover, Wallenius Wilhelmsen is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 40% over the next three years. However, Wallenius Wilhelmsen's future ROE is expected to decline to 18% despite the expected decline in its payout ratio. We infer that there could be other factors that could be steering the foreseen decline in the company's ROE.

Summary

On the whole, we feel that Wallenius Wilhelmsen's performance has been quite good. Especially the high ROE, Which has contributed to the impressive growth seen in earnings. Despite the company reinvesting only a small portion of its profits, it still has managed to grow its earnings so that is appreciable. That being so, according to the latest industry analyst forecasts, the company's earnings are expected to shrink in the future. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Valuation is complex, but we're here to simplify it.

Discover if Wallenius Wilhelmsen might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:WAWI

Wallenius Wilhelmsen

Engages in the logistics and transportation business worldwide.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives