This Is Why Norwegian Air Shuttle ASA's (OB:NAS) CEO Can Expect A Bump Up In Their Pay Packet

Key Insights

- Norwegian Air Shuttle will host its Annual General Meeting on 14th of May

- Salary of kr5.94m is part of CEO Geir Karlsen's total remuneration

- The total compensation is 31% less than the average for the industry

- Over the past three years, Norwegian Air Shuttle's EPS fell by 29% and over the past three years, the total shareholder return was 29%

Shareholders will be pleased by the robust performance of Norwegian Air Shuttle ASA (OB:NAS) recently and this will be kept in mind in the upcoming AGM on 14th of May. They will probably be more interested in hearing the board discuss future initiatives to further improve the business as they vote on resolutions such as executive remuneration. In our analysis below, we discuss why we think the CEO compensation looks acceptable and the case for a raise.

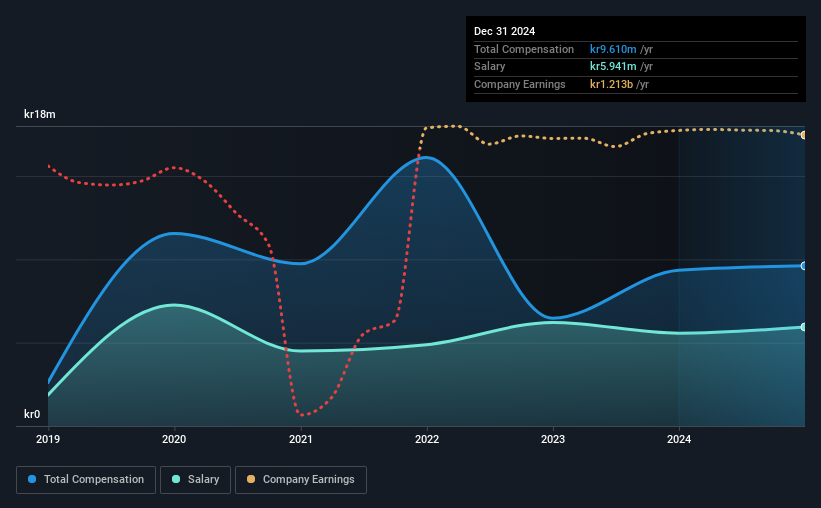

See our latest analysis for Norwegian Air Shuttle

How Does Total Compensation For Geir Karlsen Compare With Other Companies In The Industry?

At the time of writing, our data shows that Norwegian Air Shuttle ASA has a market capitalization of kr14b, and reported total annual CEO compensation of kr9.6m for the year to December 2024. This means that the compensation hasn't changed much from last year. We note that the salary portion, which stands at kr5.94m constitutes the majority of total compensation received by the CEO.

On comparing similar companies from the Norway Airlines industry with market caps ranging from kr10b to kr33b, we found that the median CEO total compensation was kr14m. That is to say, Geir Karlsen is paid under the industry median. Furthermore, Geir Karlsen directly owns kr9.4m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | kr5.9m | kr5.6m | 62% |

| Other | kr3.7m | kr3.8m | 38% |

| Total Compensation | kr9.6m | kr9.3m | 100% |

Speaking on an industry level, nearly 32% of total compensation represents salary, while the remainder of 68% is other remuneration. Norwegian Air Shuttle pays out 62% of remuneration in the form of a salary, significantly higher than the industry average. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Norwegian Air Shuttle ASA's Growth

Over the last three years, Norwegian Air Shuttle ASA has shrunk its earnings per share by 29% per year. It achieved revenue growth of 38% over the last year.

The reduction in EPS, over three years, is arguably concerning. On the other hand, the strong revenue growth suggests the business is growing. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Norwegian Air Shuttle ASA Been A Good Investment?

With a total shareholder return of 29% over three years, Norwegian Air Shuttle ASA shareholders would, in general, be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

While the company seems to be headed in the right direction performance-wise, there's always room for improvement. If it continues on the same road, shareholders might feel even more confident about their investment, and have little to no objections concerning CEO pay. Rather, investors would more likely want to engage on discussions related to key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 1 warning sign for Norwegian Air Shuttle that investors should look into moving forward.

Switching gears from Norwegian Air Shuttle, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Norwegian Air Shuttle might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:NAS

Norwegian Air Shuttle

Provides air travel services in Norway and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives