Advertisement

These 4 Measures Indicate That LINK Mobility Group Holding (OB:LINK) Is Using Debt Reasonably Well

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that LINK Mobility Group Holding ASA (OB:LINK) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for LINK Mobility Group Holding

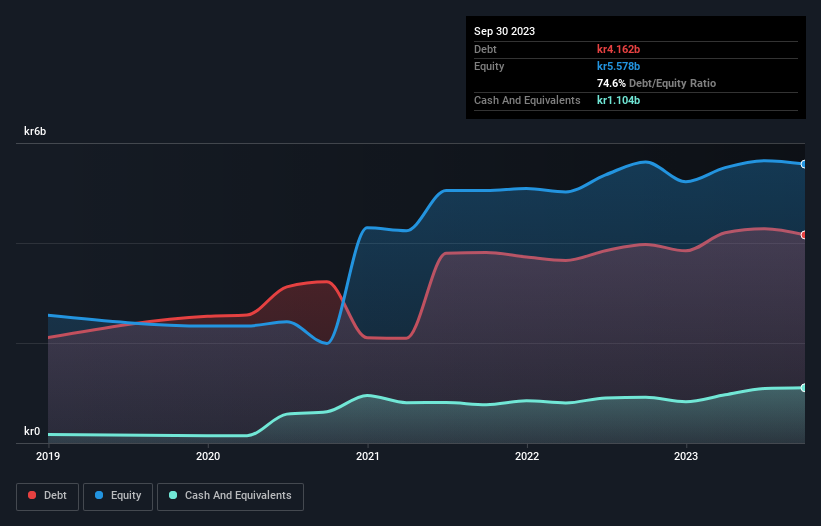

What Is LINK Mobility Group Holding's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2023 LINK Mobility Group Holding had kr4.16b of debt, an increase on kr3.97b, over one year. However, it does have kr1.10b in cash offsetting this, leading to net debt of about kr3.06b.

How Strong Is LINK Mobility Group Holding's Balance Sheet?

The latest balance sheet data shows that LINK Mobility Group Holding had liabilities of kr1.53b due within a year, and liabilities of kr4.64b falling due after that. Offsetting this, it had kr1.10b in cash and kr1.40b in receivables that were due within 12 months. So it has liabilities totalling kr3.67b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of kr5.05b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Weak interest cover of 1.1 times and a disturbingly high net debt to EBITDA ratio of 5.2 hit our confidence in LINK Mobility Group Holding like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. Looking on the bright side, LINK Mobility Group Holding boosted its EBIT by a silky 74% in the last year. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine LINK Mobility Group Holding's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, LINK Mobility Group Holding actually produced more free cash flow than EBIT over the last two years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

LINK Mobility Group Holding's interest cover was a real negative on this analysis, as was its net debt to EBITDA. But like a ballerina ending on a perfect pirouette, it has not trouble converting EBIT to free cash flow. Looking at all this data makes us feel a little cautious about LINK Mobility Group Holding's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that LINK Mobility Group Holding is showing 1 warning sign in our investment analysis , you should know about...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:LINK

LINK Mobility Group Holding

Provides mobile and communication-platform-as-a-service solutions.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor