Stock Analysis

- Norway

- /

- Oil and Gas

- /

- OB:BWE

Analysts Just Shipped A Captivating Upgrade To Their BW Energy Limited (OB:BWE) Estimates

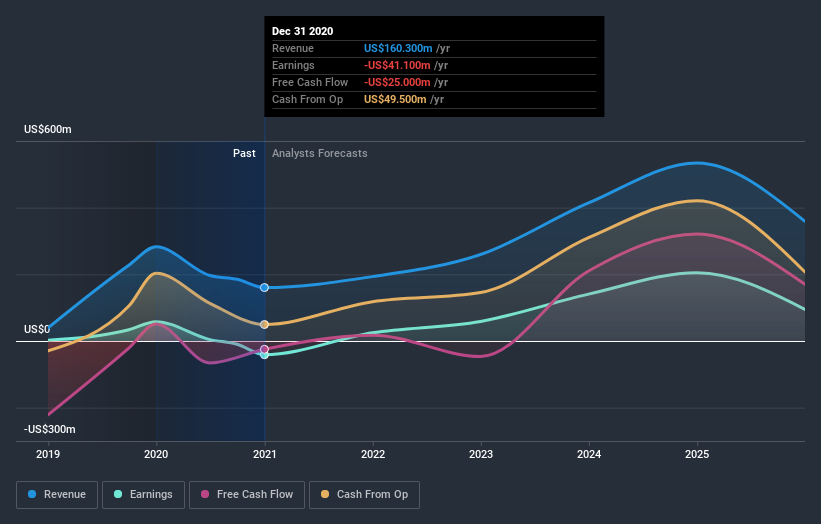

BW Energy Limited (OB:BWE) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with analysts modelling a real improvement in business performance.

After this upgrade, BW Energy's four analysts are now forecasting revenues of US$225m in 2021. This would be a sizeable 40% improvement in sales compared to the last 12 months. The losses are expected to disappear over the next year or so, with forecasts for a profit of US$0.11 per share this year. Previously, the analysts had been modelling revenues of US$193m and earnings per share (EPS) of US$0.09 in 2021. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

View our latest analysis for BW Energy

Although the analysts have upgraded their earnings estimates, there was no change to the consensus price target of US$3.97, suggesting that the forecast performance does not have a long term impact on the company's valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values BW Energy at US$45.00 per share, while the most bearish prices it at US$24.32. We would probably assign less value to the forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. For example, we noticed that BW Energy's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 40% growth to the end of 2021 on an annualised basis. That is well above its historical decline of 43% a year over the past year. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 7.4% annually. Not only are BW Energy's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. The lack of change in the price target is puzzling, but with a serious upgrade to this year's earnings expectations, it might be time to take another look at BW Energy.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple BW Energy analysts - going out to 2025, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you’re looking to trade BW Energy, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether BW Energy is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OB:BWE

BW Energy

An exploration and production company, engages in the acquisition, development, and production of oil and natural gas fields in Gabon and Brazil.

Undervalued with high growth potential.