Advertisement

- Norway

- /

- Aerospace & Defense

- /

- OB:NTI

The one-year returns have been for Norsk Titanium (OB:NTI) shareholders despite underlying losses increasing

Over the last month the Norsk Titanium AS (OB:NTI) has been much stronger than before, rebounding by 246%.

The recent uptick of 207% could be a positive sign of things to come, so let's take a look at historical fundamentals.

View our latest analysis for Norsk Titanium

Norsk Titanium recorded just US$2,502,000 in revenue over the last twelve months, which isn't really enough for us to consider it to have a proven product. You have to wonder why venture capitalists aren't funding it. So it seems that the investors focused more on what could be, than paying attention to the current revenues (or lack thereof). It seems likely some shareholders believe that Norsk Titanium will significantly advance the business plan before too long.

Companies that lack both meaningful revenue and profits are usually considered high risk. We can see that they needed to raise more capital, and took that step recently despite the fact that it would have been dilutive to current holders. While some such companies go on to make revenue, profits, and generate value, others get hyped up by hopeful naifs before eventually going bankrupt.

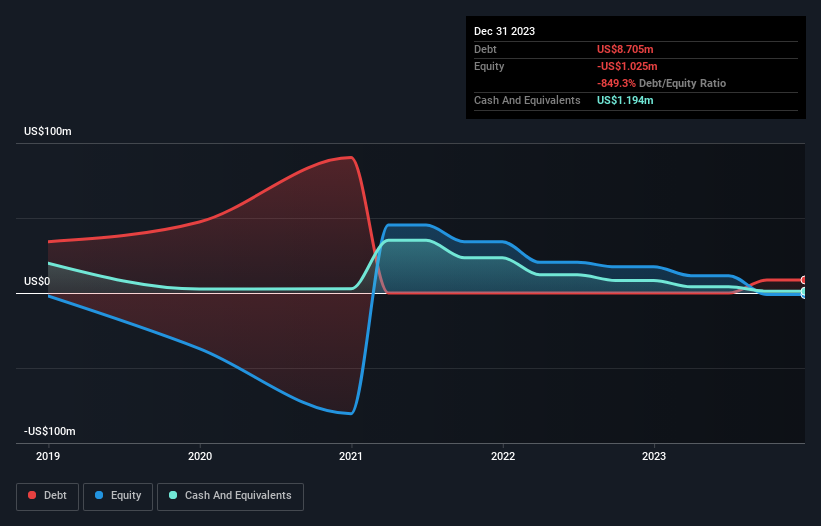

Our data indicates that Norsk Titanium had more in total liabilities than it had cash, when it last reported. That made it extremely high risk, in our view. But since the share price has dived 13% in the last year , it looks like some investors think it's time to abandon ship, so to speak, even though the cash reserves look a little better with the capital raising. The image below shows how Norsk Titanium's balance sheet has changed over time; if you want to see the precise values, simply click on the image.

It can be extremely risky to invest in a company that doesn't even have revenue. There's no way to know its value easily. What if insiders are ditching the stock hand over fist? I would feel more nervous about the company if that were so. It only takes a moment for you to check whether we have identified any insider sales recently.

What About The Total Shareholder Return (TSR)?

Investors should note that there's a difference between Norsk Titanium's total shareholder return (TSR) and its share price change, which we've covered above. The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. We note that Norsk Titanium's TSR, at 27% is higher than its share price return of -13%. When you consider it hasn't been paying a dividend, this data suggests shareholders have benefitted from a spin-off, or had the opportunity to acquire attractively priced shares in a discounted capital raising.

A Different Perspective

It's nice to see that Norsk Titanium shareholders have gained 27% over the last year. And the share price momentum remains respectable, with a gain of 61% in the last three months. This suggests the company is continuing to win over new investors. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Take risks, for example - Norsk Titanium has 4 warning signs (and 3 which don't sit too well with us) we think you should know about.

Of course Norsk Titanium may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Norwegian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Norsk Titanium might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:NTI

Norsk Titanium

Engages in 3D printing of metal alloys for commercial aerospace, defense, and industrial sectors in Europe and the United States.

Exceptional growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor