Advertisement

- Norway

- /

- Construction

- /

- OB:IWS

IWS (OB:IWS): Net Margin Jumps to 15.7% Challenges Market Skepticism on Profitability

Simply Wall St

Reviewed by Simply Wall St

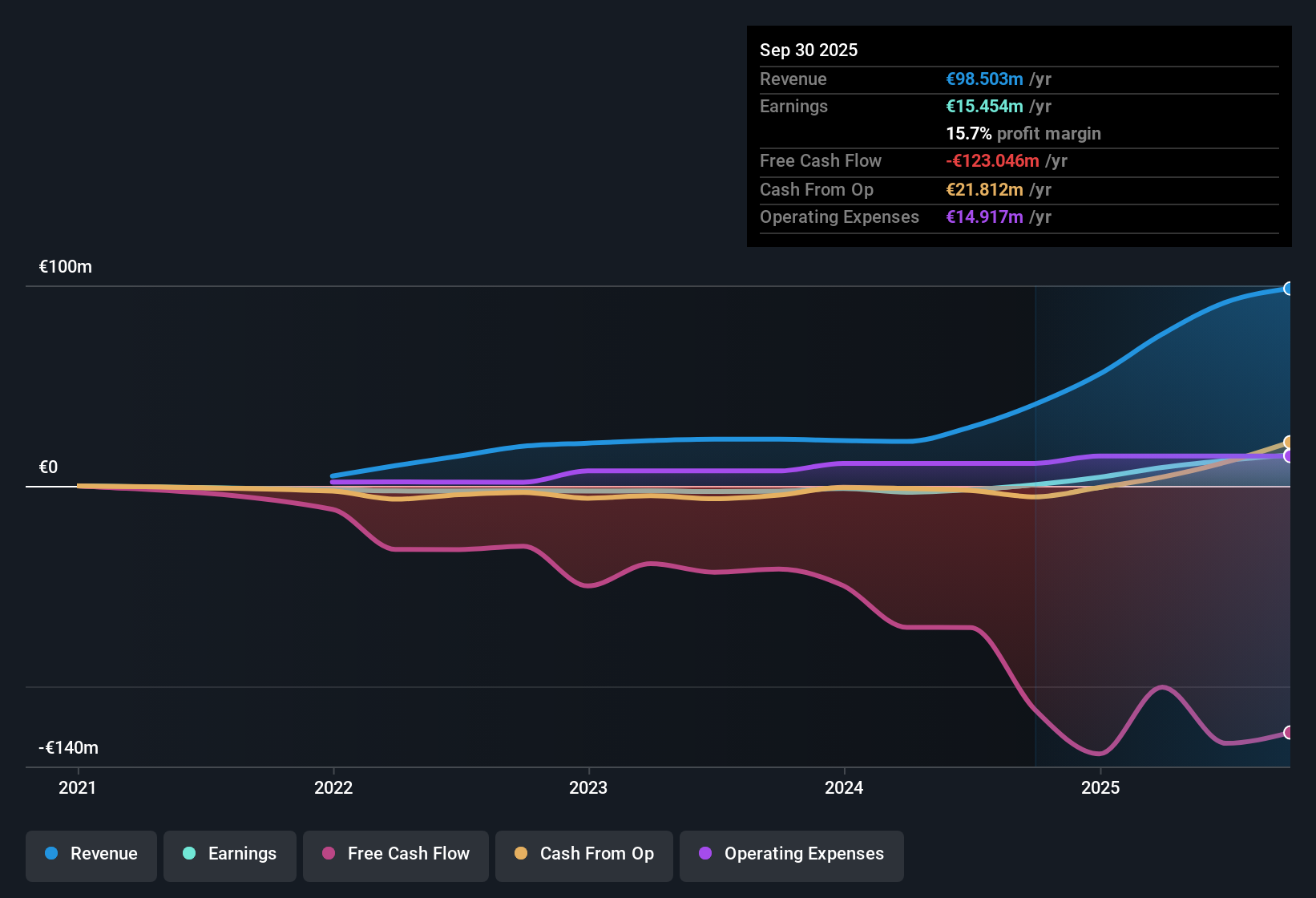

Integrated Wind Solutions (OB:IWS) just released its Q3 2025 results, posting total revenue of €24.1 million and net income of €4.7 million for the period, with EPS at €0.12. Over the past year, the company has seen revenue climb from €40.7 million in Q3 2024 to €98.5 million in the latest trailing twelve months, while net income increased from €0.6 million to €15.5 million for that same period. Solid margins round out the report, giving investors plenty to consider as they look for signals in the company’s recent performance.

See our full analysis for Integrated Wind Solutions.Next, we will set these results against the prevailing narratives and examine which parts of the story hold up, as well as where market expectations might need to be reconsidered.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margins Rise to 15.7%

- Net profit margin for the last twelve months reached 15.7%, up from 1.4% a year earlier. This shows that a much larger slice of every euro in revenue is now turning into profit.

- What’s notable is how this margin expansion heavily supports optimism from analysts:

- Revenue in the trailing twelve months rose to €98.5 million, and net income jumped to €15.5 million, outstripping the Norwegian market’s expected growth rates.

- Analysts' consensus narrative points out that this level of profitability is uncommon for a company expanding at a 12% annual clip, strengthening the argument that IWS is executing well on both growth and efficiency.

- Solid margin expansion and profits like these make this earnings season harder to ignore. See how consensus thinks this changes the story. 📊 Read the full Integrated Wind Solutions Consensus Narrative.

Valuation Still Below Peers

- The price-to-earnings ratio stands at 9.3x, which is lower than the European Construction industry average of 13.9x and peer companies at 13.1x, while the current share price is €42.50.

- Consensus narrative highlights IWS’s below-average valuation as a key point:

- Despite strong recent profit growth, IWS trades at a steep 73.8% discount to its DCF fair value of €162.12. This stands out for those used to premium multiples for companies showing this sort of momentum.

- This discount versus both peers and a calculated fair value offers a buffer and could attract value-focused investors, though the narrative notes that the mix of non-cash earnings means not all reported profits may be of the highest quality.

Rapid EPS Expansion Outpaces Market

- Basic EPS for the trailing twelve months hit €0.39, a massive jump from €0.01 in the same period last year, supported by a 2,587.7% earnings growth rate year-on-year.

- The consensus narrative observes a rare combination. EPS and earnings growth rates here are far above both the Norwegian market’s 16.3% average for earnings and 2.6% average for revenues:

- These figures challenge the common perception that rapid top-line growth comes at the expense of profitability. For IWS, expansion hasn't eroded margins.

- Consensus notes that this outperformance means bulls have solid ground, but investors still need to watch for risks linked to operating cash flow coverage and the quality of earnings going forward.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Integrated Wind Solutions's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

While IWS's rapid growth and impressive EPS expansion stand out, concerns remain regarding the consistency and quality of its earnings given some reliance on non-cash items and questions about ongoing cash flow coverage.

If you want more confidence in sustained growth and stable financials, check out stable growth stocks screener (2073 results) to find companies with a proven record of reliable results through varying market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:IWS

Integrated Wind Solutions

Through its subsidiaries, provides offshore wind services in the United Kingdom, the Netherlands, Taiwan, Poland, Belgium, Greece, France, Denmark, Norway, and internationally.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative