Advertisement

Havyard Group (OB:HYARD) Knows How To Allocate Capital Effectively

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. With that in mind, the ROCE of Havyard Group (OB:HYARD) looks great, so lets see what the trend can tell us.

Return On Capital Employed (ROCE): What is it?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Havyard Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.28 = kr110m ÷ (kr1.5b - kr1.1b) (Based on the trailing twelve months to June 2021).

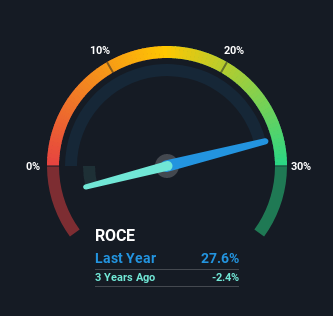

So, Havyard Group has an ROCE of 28%. On its own that's a fantastic return on capital, though it's the same as the Machinery industry average of 28%.

View our latest analysis for Havyard Group

Historical performance is a great place to start when researching a stock so above you can see the gauge for Havyard Group's ROCE against it's prior returns. If you'd like to look at how Havyard Group has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

It's great to see that Havyard Group has started to generate some pre-tax earnings from prior investments. The company was generating losses five years ago, but now it's turned around, earning 28% which is no doubt a relief for some early shareholders. At first glance, it seems the business is getting more proficient at generating returns, because over the same period, the amount of capital employed has reduced by 50%. Havyard Group could be selling under-performing assets since the ROCE is improving.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. The current liabilities has increased to 74% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. And with current liabilities at those levels, that's pretty high.

The Bottom Line On Havyard Group's ROCE

In the end, Havyard Group has proven it's capital allocation skills are good with those higher returns from less amount of capital. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 53% return over the last five years. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

Havyard Group does come with some risks though, we found 3 warning signs in our investment analysis, and 2 of those are significant...

High returns are a key ingredient to strong performance, so check out our free list ofstocks earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if Eqva might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OB:EQVA

Eqva

Provides technical solutions and services to maritime and land based industries in Norway and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor