Advertisement

- Norway

- /

- Industrials

- /

- OB:BONHR

Bonheur ASA Just Missed EPS By 28%: Here's What Analysts Think Will Happen Next

As you might know, Bonheur ASA (OB:BONHR) last week released its latest first-quarter, and things did not turn out so great for shareholders. Results showed a clear earnings miss, with kr3.0b revenue coming in 6.0% lower than what the analystsexpected. Statutory earnings per share (EPS) of kr4.00 missed the mark badly, arriving some 28% below what was expected. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for Bonheur

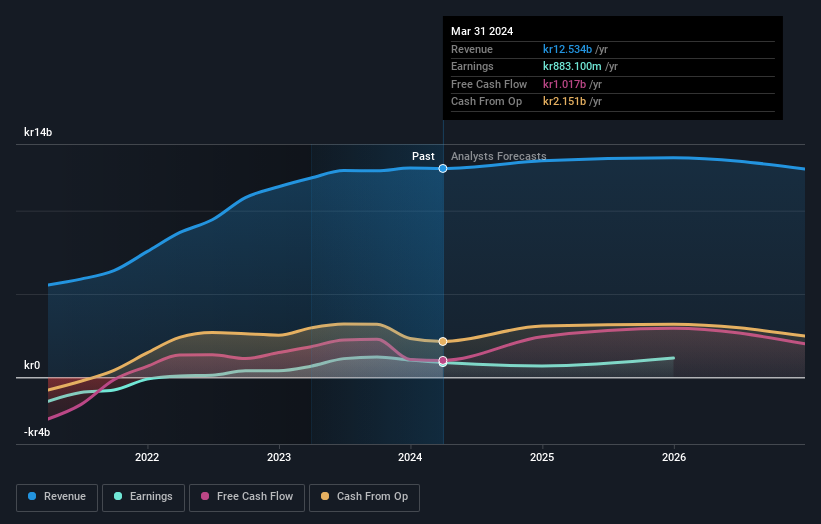

Taking into account the latest results, the current consensus from Bonheur's two analysts is for revenues of kr13.0b in 2024. This would reflect a modest 3.6% increase on its revenue over the past 12 months. Statutory earnings per share are expected to crater 23% to kr16.08 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of kr13.0b and earnings per share (EPS) of kr9.96 in 2024. There was no real change to the revenue estimates, but the analysts do seem more bullish on earnings, given the considerable lift to earnings per share expectations following these results.

The consensus price target was unchanged at kr318, implying that the improved earnings outlook is not expected to have a long term impact on value creation for shareholders.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that Bonheur's revenue growth is expected to slow, with the forecast 4.9% annualised growth rate until the end of 2024 being well below the historical 15% p.a. growth over the last five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 5.2% annually. Factoring in the forecast slowdown in growth, it looks like Bonheur is forecast to grow at about the same rate as the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Bonheur following these results. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. The consensus price target held steady at kr318, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have analyst estimates for Bonheur going out as far as 2026, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Bonheur (1 is a bit unpleasant!) that you need to be mindful of.

Valuation is complex, but we're here to simplify it.

Discover if Bonheur might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:BONHR

Bonheur

Engages in the renewable energy, wind service, and cruise businesses in the United Kingdom, Norway, Europe, Asia, the Americas, Africa, and Internationally.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor