Advertisement

- Netherlands

- /

- Beverage

- /

- ENXTAM:CCEP

We Think Some Shareholders May Hesitate To Increase Coca-Cola Europacific Partners PLC's (AMS:CCEP) CEO Compensation

Key Insights

- Coca-Cola Europacific Partners will host its Annual General Meeting on 22nd of May

- CEO Damian Gammell's total compensation includes salary of €1.52m

- The total compensation is 178% higher than the average for the industry

- Over the past three years, Coca-Cola Europacific Partners' EPS grew by 13% and over the past three years, the total shareholder return was 75%

Under the guidance of CEO Damian Gammell, Coca-Cola Europacific Partners PLC (AMS:CCEP) has performed reasonably well recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 22nd of May. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

View our latest analysis for Coca-Cola Europacific Partners

How Does Total Compensation For Damian Gammell Compare With Other Companies In The Industry?

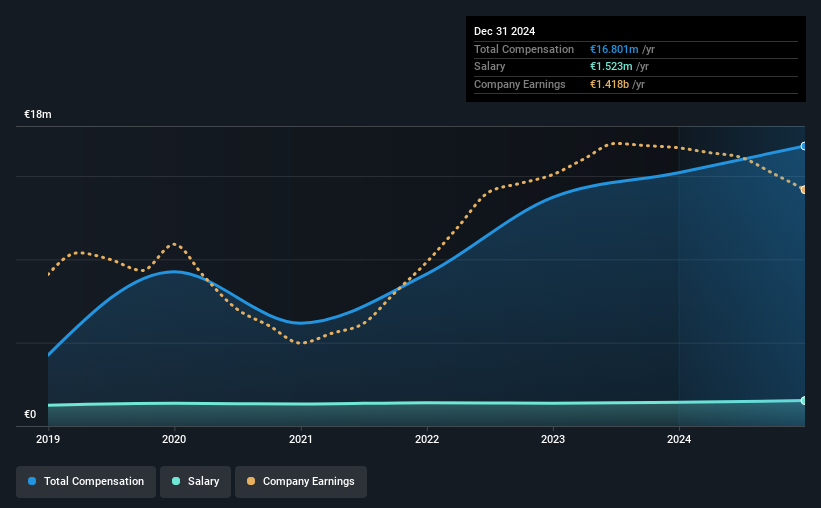

According to our data, Coca-Cola Europacific Partners PLC has a market capitalization of €36b, and paid its CEO total annual compensation worth €17m over the year to December 2024. That's a notable increase of 11% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at €1.5m.

In comparison with other companies in the the Netherlands Beverage industry with market capitalizations over €7.2b, the reported median total CEO compensation was €6.1m. Accordingly, our analysis reveals that Coca-Cola Europacific Partners PLC pays Damian Gammell north of the industry median. Moreover, Damian Gammell also holds €41m worth of Coca-Cola Europacific Partners stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | €1.5m | €1.4m | 9% |

| Other | €15m | €14m | 91% |

| Total Compensation | €17m | €15m | 100% |

Speaking on an industry level, nearly 54% of total compensation represents salary, while the remainder of 46% is other remuneration. Coca-Cola Europacific Partners sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Coca-Cola Europacific Partners PLC's Growth Numbers

Coca-Cola Europacific Partners PLC has seen its earnings per share (EPS) increase by 13% a year over the past three years. It achieved revenue growth of 12% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Coca-Cola Europacific Partners PLC Been A Good Investment?

Boasting a total shareholder return of 75% over three years, Coca-Cola Europacific Partners PLC has done well by shareholders. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 3 warning signs for Coca-Cola Europacific Partners that investors should look into moving forward.

Switching gears from Coca-Cola Europacific Partners, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTAM:CCEP

Coca-Cola Europacific Partners

Produces, distributes, and sells a range of non-alcoholic ready to drink beverages.

Slightly overvalued with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor