Advertisement

- Netherlands

- /

- Professional Services

- /

- ENXTAM:MORE

Shareholders Would Enjoy A Repeat Of Morefield Group's (AMS:MORE) Recent Growth In Returns

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Speaking of which, we noticed some great changes in Morefield Group's (AMS:MORE) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Morefield Group is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

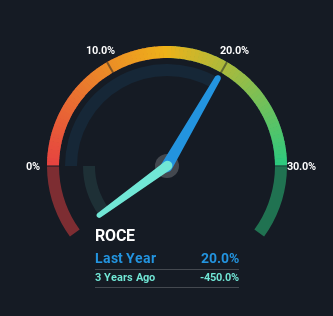

0.20 = €5.8m ÷ (€54m - €25m) (Based on the trailing twelve months to June 2023).

Therefore, Morefield Group has an ROCE of 20%. In absolute terms that's a great return and it's even better than the Professional Services industry average of 16%.

See our latest analysis for Morefield Group

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Morefield Group has performed in the past in other metrics, you can view this free graph of Morefield Group's past earnings, revenue and cash flow.

How Are Returns Trending?

We like the trends that we're seeing from Morefield Group. The numbers show that in the last five years, the returns generated on capital employed have grown considerably to 20%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 28%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

One more thing to note, Morefield Group has decreased current liabilities to 46% of total assets over this period, which effectively reduces the amount of funding from suppliers or short-term creditors. So shareholders would be pleased that the growth in returns has mostly come from underlying business performance. However, current liabilities are still at a pretty high level, so just be aware that this can bring with it some risks.

The Key Takeaway

In summary, it's great to see that Morefield Group can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. Since the stock has returned a solid 64% to shareholders over the last five years, it's fair to say investors are beginning to recognize these changes. In light of that, we think it's worth looking further into this stock because if Morefield Group can keep these trends up, it could have a bright future ahead.

One more thing, we've spotted 4 warning signs facing Morefield Group that you might find interesting.

Morefield Group is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTAM:MORE

Morefield Group

Through its subsidiaries, engages in selecting, advising, supplying, and maintaining aids for people with a physical disability in Curaçao.

Slight risk with acceptable track record.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor