Advertisement

- Malaysia

- /

- Other Utilities

- /

- KLSE:YTLPOWR

Why We Think YTL Power International Berhad's (KLSE:YTLPOWR) CEO Compensation Is Not Excessive At All

CEO Seok Yeoh has done a decent job of delivering relatively good performance at YTL Power International Berhad (KLSE:YTLPOWR) recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 06 December 2022. Here is our take on why we think the CEO compensation looks appropriate.

Our analysis indicates that YTLPOWR is potentially undervalued!

How Does Total Compensation For Seok Yeoh Compare With Other Companies In The Industry?

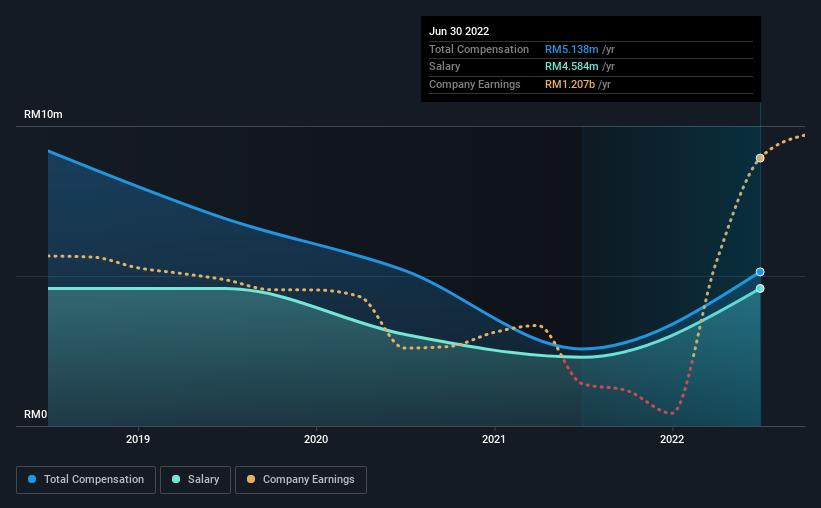

Our data indicates that YTL Power International Berhad has a market capitalization of RM5.8b, and total annual CEO compensation was reported as RM5.1m for the year to June 2022. We note that's an increase of 100% above last year. In particular, the salary of RM4.58m, makes up a huge portion of the total compensation being paid to the CEO.

On examining similar-sized companies in the industry with market capitalizations between RM4.5b and RM14b, we discovered that the median CEO total compensation of that group was RM5.9m. This suggests that YTL Power International Berhad remunerates its CEO largely in line with the industry average. What's more, Seok Yeoh holds RM100m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | RM4.6m | RM2.3m | 89% |

| Other | RM554k | RM278k | 11% |

| Total Compensation | RM5.1m | RM2.6m | 100% |

Talking in terms of the industry, salary represented approximately 25% of total compensation out of all the companies we analyzed, while other remuneration made up 75% of the pie. According to our research, YTL Power International Berhad has allocated a higher percentage of pay to salary in comparison to the wider industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at YTL Power International Berhad's Growth Numbers

YTL Power International Berhad has seen its earnings per share (EPS) increase by 45% a year over the past three years. Its revenue is up 61% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The combination of strong revenue growth with medium-term EPS improvement certainly points to the kind of growth we like to see. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has YTL Power International Berhad Been A Good Investment?

With a total shareholder return of 16% over three years, YTL Power International Berhad shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 3 warning signs for YTL Power International Berhad (2 shouldn't be ignored!) that you should be aware of before investing here.

Important note: YTL Power International Berhad is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:YTLPOWR

YTL Power International Berhad

An investment holding company, provides electricity, clean water, sewerage system, and telecommunication services in Malaysia, Singapore, the United Kingdom, and internationally.

Undervalued with questionable track record.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|30.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|25.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|63.2% undervalued

ME

Community Contributor