Advertisement

- Malaysia

- /

- Electric Utilities

- /

- KLSE:TENAGA

Tenaga Nasional Berhad (KLSE:TENAGA) Takes On Some Risk With Its Use Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Tenaga Nasional Berhad (KLSE:TENAGA) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Tenaga Nasional Berhad

What Is Tenaga Nasional Berhad's Net Debt?

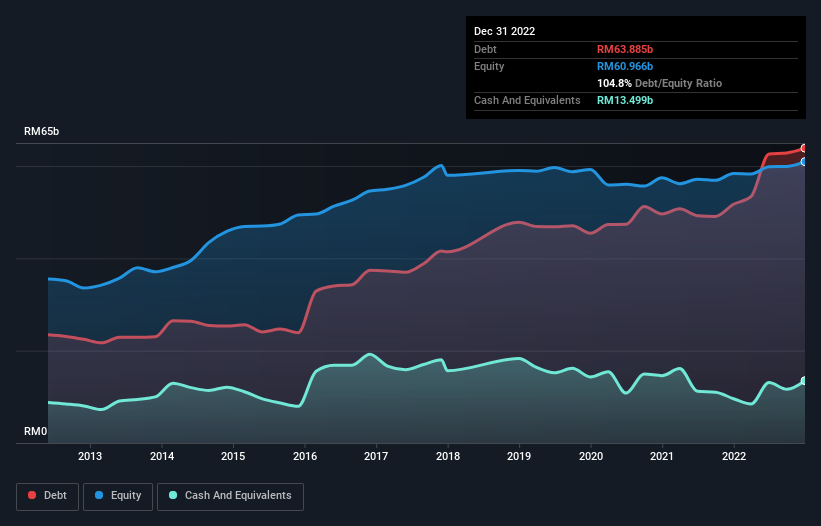

The image below, which you can click on for greater detail, shows that at December 2022 Tenaga Nasional Berhad had debt of RM63.9b, up from RM51.7b in one year. On the flip side, it has RM13.5b in cash leading to net debt of about RM50.4b.

A Look At Tenaga Nasional Berhad's Liabilities

Zooming in on the latest balance sheet data, we can see that Tenaga Nasional Berhad had liabilities of RM37.6b due within 12 months and liabilities of RM107.4b due beyond that. On the other hand, it had cash of RM13.5b and RM27.5b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM104.0b.

The deficiency here weighs heavily on the RM55.7b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Tenaga Nasional Berhad would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Tenaga Nasional Berhad's debt to EBITDA ratio (3.1) suggests that it uses some debt, its interest cover is very weak, at 2.4, suggesting high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. On a slightly more positive note, Tenaga Nasional Berhad grew its EBIT at 16% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Tenaga Nasional Berhad can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Tenaga Nasional Berhad recorded free cash flow worth 62% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Mulling over Tenaga Nasional Berhad's attempt at staying on top of its total liabilities, we're certainly not enthusiastic. But at least it's pretty decent at growing its EBIT; that's encouraging. We should also note that Electric Utilities industry companies like Tenaga Nasional Berhad commonly do use debt without problems. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Tenaga Nasional Berhad stock a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Tenaga Nasional Berhad has 3 warning signs (and 1 which is concerning) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Tenaga Nasional Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TENAGA

Tenaga Nasional Berhad

Engages in the generation, transmission, distribution, and sale of electricity in Malaysia, the United Kingdom, Kuwait, the Republic of Ireland, Australia, and internationally.

Very undervalued with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets