The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Tenaga Nasional Berhad (KLSE:TENAGA) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Our analysis indicates that TENAGA is potentially undervalued!

What Is Tenaga Nasional Berhad's Net Debt?

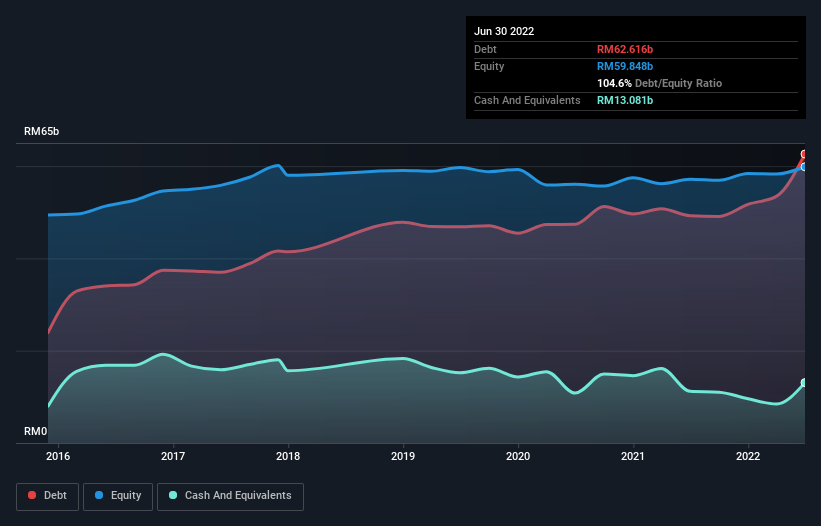

The image below, which you can click on for greater detail, shows that at June 2022 Tenaga Nasional Berhad had debt of RM62.6b, up from RM49.2b in one year. However, it does have RM13.1b in cash offsetting this, leading to net debt of about RM49.5b.

How Strong Is Tenaga Nasional Berhad's Balance Sheet?

The latest balance sheet data shows that Tenaga Nasional Berhad had liabilities of RM35.0b due within a year, and liabilities of RM107.6b falling due after that. On the other hand, it had cash of RM13.1b and RM24.5b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM105.0b.

This deficit casts a shadow over the RM47.6b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Tenaga Nasional Berhad would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Tenaga Nasional Berhad's debt to EBITDA ratio (3.2) suggests that it uses some debt, its interest cover is very weak, at 2.3, suggesting high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. On a slightly more positive note, Tenaga Nasional Berhad grew its EBIT at 14% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Tenaga Nasional Berhad's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Tenaga Nasional Berhad recorded free cash flow worth 79% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Tenaga Nasional Berhad's level of total liabilities was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example its conversion of EBIT to free cash flow was refreshing. It's also worth noting that Tenaga Nasional Berhad is in the Electric Utilities industry, which is often considered to be quite defensive. Taking the abovementioned factors together we do think Tenaga Nasional Berhad's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Tenaga Nasional Berhad you should be aware of, and 1 of them is concerning.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Tenaga Nasional Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TENAGA

Tenaga Nasional Berhad

Engages in the generation, transmission, distribution, and sale of electricity in Malaysia and internationally.

Proven track record average dividend payer.