Advertisement

- China

- /

- Semiconductors

- /

- SHSE:603501

Spotlight On 3 Leading Growth Companies With High Insider Ownership

Simply Wall St

Reviewed by Simply Wall St

In a week marked by market volatility and concerns over economic growth, investors are seeking stability and potential upside in their portfolios. Amid these fluctuations, growth companies with high insider ownership can offer unique advantages, as they often indicate strong confidence from those who know the business best. In this article, we spotlight three leading growth companies where significant insider ownership aligns with robust business prospects, making them compelling considerations for discerning investors navigating today's uncertain market landscape.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.2% |

| Gaming Innovation Group (OB:GIG) | 26.7% | 37.4% |

| KebNi (OM:KEBNI B) | 37.8% | 90.4% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 36.4% |

| Global Tax Free (KOSDAQ:A204620) | 18.1% | 90.6% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.4% | 60.9% |

| Calliditas Therapeutics (OM:CALTX) | 12.7% | 53.7% |

| Adocia (ENXTPA:ADOC) | 11.9% | 63% |

| Vow (OB:VOW) | 31.7% | 97.7% |

| UTI (KOSDAQ:A179900) | 33.1% | 122.7% |

Here's a peek at a few of the choices from the screener.

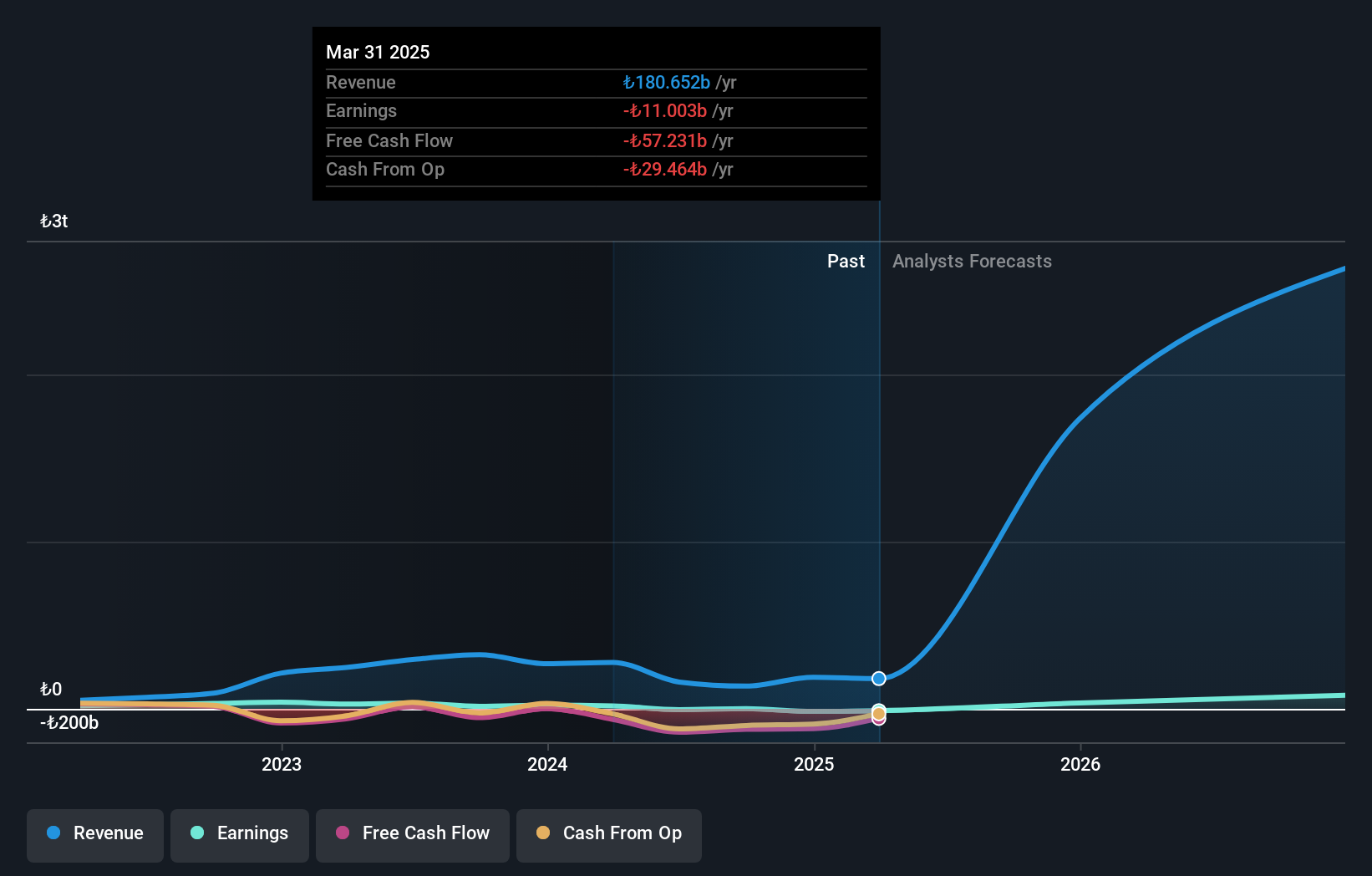

Haci Ömer Sabanci Holding (IBSE:SAHOL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Haci Ömer Sabanci Holding A.S. operates primarily in the finance, manufacturing, and trading sectors worldwide, with a market cap of TRY192.60 billion.

Operations: The company's revenue segments include Energy (TRY192.32 billion), Banking (TRY388.31 billion), Digital (TRY52.76 billion), Industry (TRY49.50 billion), Financial Services (TRY44.67 billion), and Construction Materials (TRY41.53 billion).

Insider Ownership: 20.5%

Earnings Growth Forecast: 83.8% p.a.

Haci Ömer Sabanci Holding exhibits strong growth potential, with revenue forecasted to grow 68.6% annually and earnings expected to increase significantly by 83.77% per year, outpacing the Turkish market. Despite a recent net loss of TRY 5.37 billion in Q1 2024, the company's price-to-earnings ratio (15.5x) remains attractive compared to the TR market (16.3x). However, shareholders have faced dilution over the past year and profit margins have declined from 11.9% to 6.8%.

- Get an in-depth perspective on Haci Ömer Sabanci Holding's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Haci Ömer Sabanci Holding shares in the market.

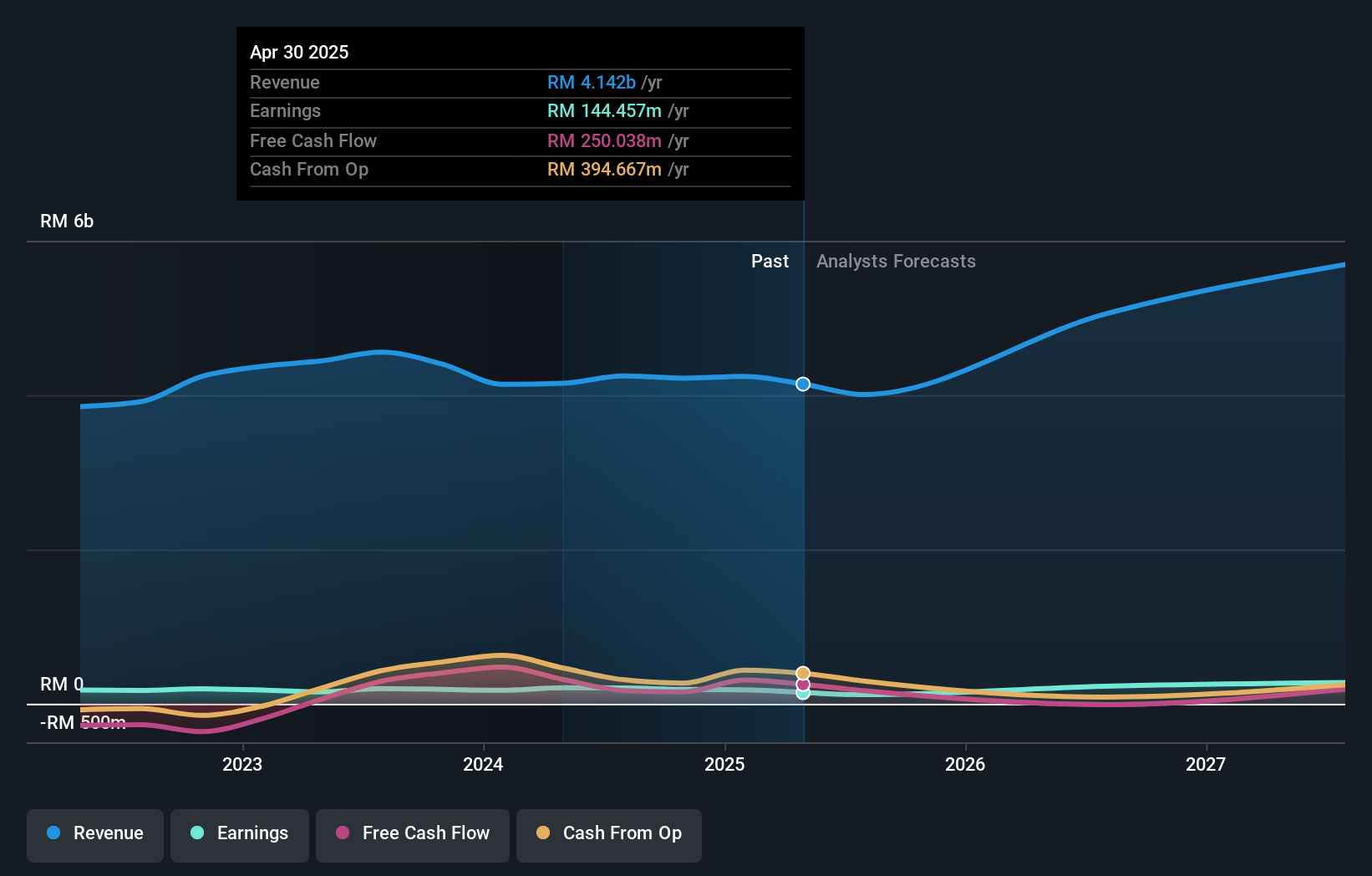

V.S. Industry Berhad (KLSE:VS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: V.S. Industry Berhad is an investment holding company involved in manufacturing, assembling, and selling electronic and electrical products as well as plastic molded components, with a market cap of MYR4.37 billion.

Operations: Revenue segments (in millions of MYR): China: 41.35, Malaysia: 3834.98, Indonesia: 322.48, Singapore: 900.14

Insider Ownership: 27.9%

Earnings Growth Forecast: 24.7% p.a.

V.S. Industry Berhad demonstrates strong growth potential with earnings forecasted to grow 24.65% annually, outpacing the Malaysian market's 12.2%. Despite slower revenue growth at 13.3%, it remains above the market average of 6.2%. The company reported a notable increase in net income for Q3 2024 (MYR 54.42 million vs MYR 26.77 million YoY). Trading at a price-to-earnings ratio of 26.6x, below the industry average, it offers good relative value despite an unstable dividend track record and low forecasted return on equity (11.6%).

- Click here to discover the nuances of V.S. Industry Berhad with our detailed analytical future growth report.

- The valuation report we've compiled suggests that V.S. Industry Berhad's current price could be quite moderate.

Will Semiconductor (SHSE:603501)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Will Semiconductor Co., Ltd., with a market cap of CN¥111.82 billion, is a semiconductor design company that provides sensor solutions, analog solutions, and touch screen and display solutions.

Operations: The company's revenue segments include sensor solutions, analog solutions, and touch screen and display solutions.

Insider Ownership: 30.7%

Earnings Growth Forecast: 47.8% p.a.

Will Semiconductor shows strong growth prospects with earnings forecasted to grow 47.8% annually, significantly outpacing the Chinese market's 22%. Revenue is expected to grow at 17.8% per year, faster than the market average of 13.5%. Despite a low forecasted return on equity (16.7%), recent earnings grew by an impressive 212.2%. Analysts predict a stock price increase of approximately 40%, reflecting positive sentiment despite no substantial insider trading activity in the past three months.

- Dive into the specifics of Will Semiconductor here with our thorough growth forecast report.

- Our expertly prepared valuation report Will Semiconductor implies its share price may be too high.

Make It Happen

- Unlock more gems! Our Fast Growing Companies With High Insider Ownership screener has unearthed 1472 more companies for you to explore.Click here to unveil our expertly curated list of 1475 Fast Growing Companies With High Insider Ownership.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603501

OmniVision Integrated Circuits Group

OmniVision Integrated Circuits Group, Inc.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor