Advertisement

Has Censof Holdings Berhad's (KLSE:CENSOF) Impressive Stock Performance Got Anything to Do With Its Fundamentals?

Censof Holdings Berhad (KLSE:CENSOF) has had a great run on the share market with its stock up by a significant 20% over the last three months. As most would know, fundamentals are what usually guide market price movements over the long-term, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. In this article, we decided to focus on Censof Holdings Berhad's ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Censof Holdings Berhad

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Censof Holdings Berhad is:

6.4% = RM6.6m ÷ RM102m (Based on the trailing twelve months to December 2023).

The 'return' is the yearly profit. That means that for every MYR1 worth of shareholders' equity, the company generated MYR0.06 in profit.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

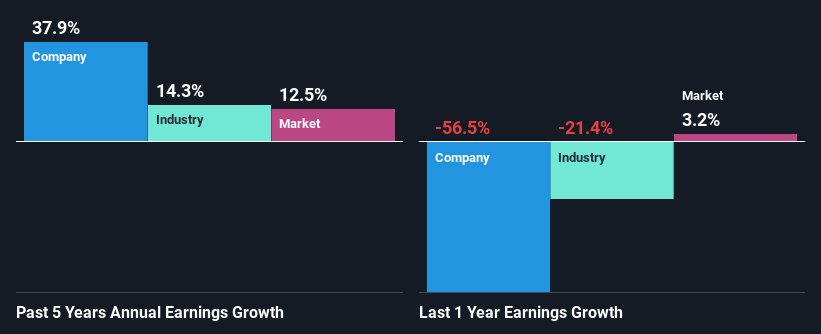

A Side By Side comparison of Censof Holdings Berhad's Earnings Growth And 6.4% ROE

At first glance, Censof Holdings Berhad's ROE doesn't look very promising. However, given that the company's ROE is similar to the average industry ROE of 7.6%, we may spare it some thought. Looking at Censof Holdings Berhad's exceptional 38% five-year net income growth in particular, we are definitely impressed. Given the slightly low ROE, it is likely that there could be some other aspects that are driving this growth. For instance, the company has a low payout ratio or is being managed efficiently.

Next, on comparing with the industry net income growth, we found that Censof Holdings Berhad's growth is quite high when compared to the industry average growth of 14% in the same period, which is great to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is Censof Holdings Berhad fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Censof Holdings Berhad Making Efficient Use Of Its Profits?

Censof Holdings Berhad has a really low three-year median payout ratio of 22%, meaning that it has the remaining 78% left over to reinvest into its business. So it looks like Censof Holdings Berhad is reinvesting profits heavily to grow its business, which shows in its earnings growth.

Additionally, Censof Holdings Berhad has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders.

Summary

In total, it does look like Censof Holdings Berhad has some positive aspects to its business. Despite its low rate of return, the fact that the company reinvests a very high portion of its profits into its business, no doubt contributed to its high earnings growth. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. Our risks dashboard would have the 3 risks we have identified for Censof Holdings Berhad.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:CENSOF

Censof Holdings Berhad

An investment holding company, engages in the design, development, implementation, and marketing of financial management software in Malaysia, Singapore, and Indonesia.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.558.3% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.1% undervalued

52 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.2% undervalued

62 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.3% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on REA Group ·

Is REA Group a Good Value Opportunity?

Fair Value:AU$14811.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on ServiceNow ·

The Company Nobody Brags About

Fair Value:US$165.6943.4% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on ASX ·

ASX Limited

Fair Value:AU$4319.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17060.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative