Advertisement

Agmo Holdings Berhad Full Year 2025 Earnings: EPS: RM0.025 (vs RM0.024 in FY 2024)

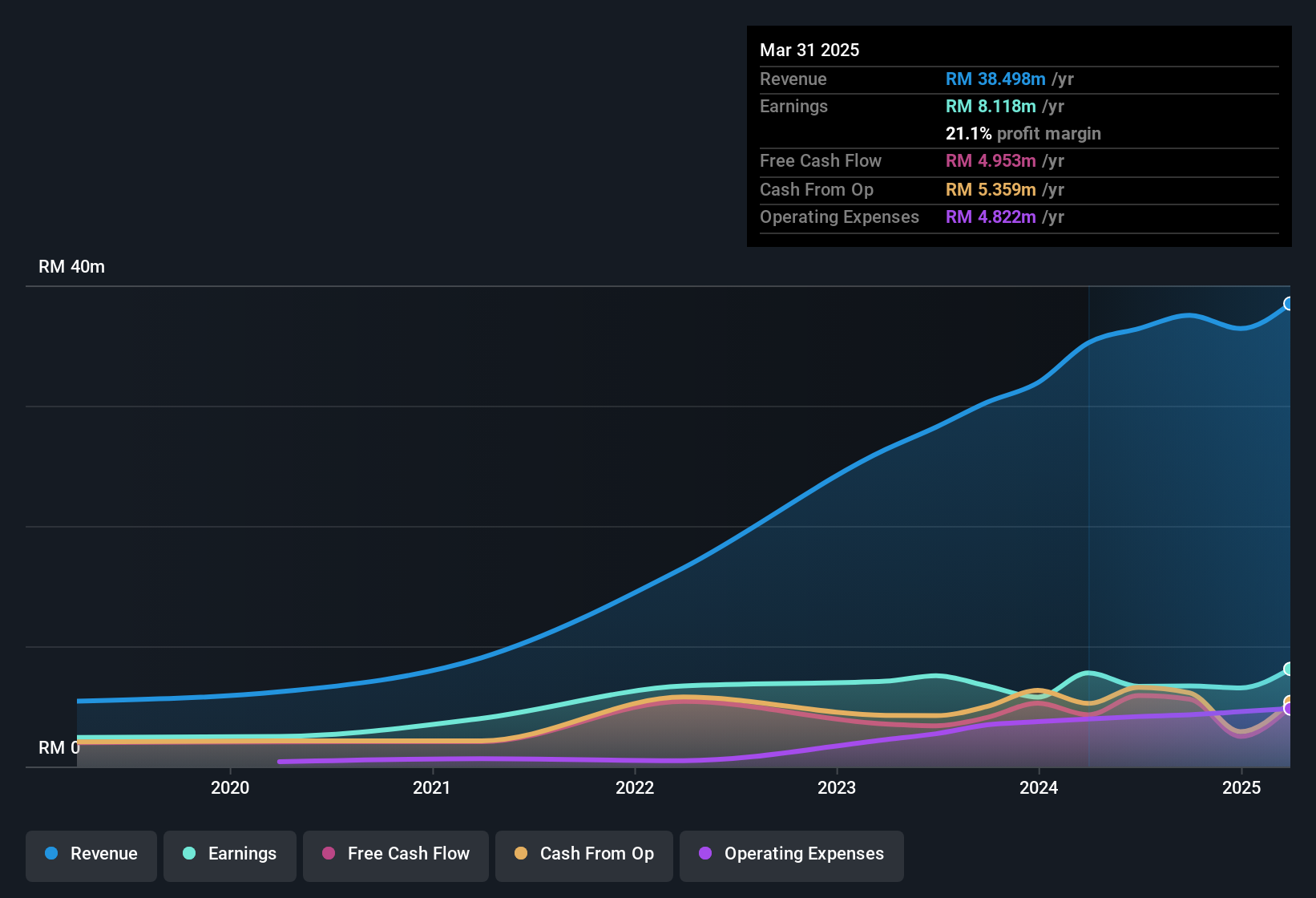

Agmo Holdings Berhad (KLSE:AGMO) Full Year 2025 Results

Key Financial Results

- Revenue: RM38.5m (up 9.3% from FY 2024).

- Net income: RM8.12m (up 4.3% from FY 2024).

- Profit margin: 21% (down from 22% in FY 2024). The decrease in margin was driven by higher expenses.

- EPS: RM0.025 (up from RM0.024 in FY 2024).

All figures shown in the chart above are for the trailing 12 month (TTM) period

Agmo Holdings Berhad's share price is broadly unchanged from a week ago.

Risk Analysis

It is worth noting though that we have found 1 warning sign for Agmo Holdings Berhad that you need to take into consideration.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:AGMO

Agmo Holdings Berhad

An investment holdings company, develops mobile and web applications in Malaysia, Hong Kong, Singapore, Sri Lanka, Cambodia, Vietnam, the People’s Republic of China, the United Kingdom, Germany, Thailand, and internationally.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|25.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|6.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|25.9% undervalued

KA

Community Contributor