Advertisement

- Malaysia

- /

- Specialty Stores

- /

- KLSE:KAMDAR

Is Kamdar Group (M) Berhad (KLSE:KAMDAR) Weighed On By Its Debt Load?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Kamdar Group (M) Berhad (KLSE:KAMDAR) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Kamdar Group (M) Berhad

What Is Kamdar Group (M) Berhad's Net Debt?

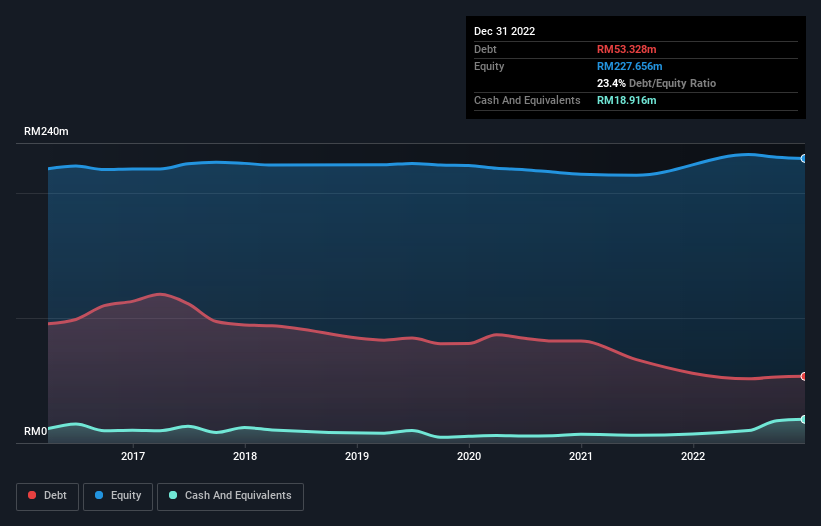

As you can see below, Kamdar Group (M) Berhad had RM53.3m of debt, at December 2022, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has RM18.9m in cash leading to net debt of about RM34.4m.

A Look At Kamdar Group (M) Berhad's Liabilities

Zooming in on the latest balance sheet data, we can see that Kamdar Group (M) Berhad had liabilities of RM24.3m due within 12 months and liabilities of RM41.5m due beyond that. On the other hand, it had cash of RM18.9m and RM6.70m worth of receivables due within a year. So its liabilities total RM40.2m more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of RM32.7m, we think shareholders really should watch Kamdar Group (M) Berhad's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Kamdar Group (M) Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Kamdar Group (M) Berhad reported revenue of RM74m, which is a gain of 9.6%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Over the last twelve months Kamdar Group (M) Berhad produced an earnings before interest and tax (EBIT) loss. Indeed, it lost RM1.2m at the EBIT level. When we look at that alongside the significant liabilities, we're not particularly confident about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. But on the bright side the company actually produced a statutory profit of RM6.0m and free cash flow of RM25m. So one might argue that there's still a chance it can get things on the right track. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Kamdar Group (M) Berhad (of which 2 are concerning!) you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Kamdar Group (M) Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KAMDAR

Kamdar Group (M) Berhad

An investment holding company, engages in the import, export, retail, and wholesale of textile and textile-based products in Malaysia.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor