Advertisement

- Malaysia

- /

- Specialty Stores

- /

- KLSE:BAUTO

These 4 Measures Indicate That Bermaz Auto Berhad (KLSE:BAUTO) Is Using Debt Extensively

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Bermaz Auto Berhad (KLSE:BAUTO) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Bermaz Auto Berhad

How Much Debt Does Bermaz Auto Berhad Carry?

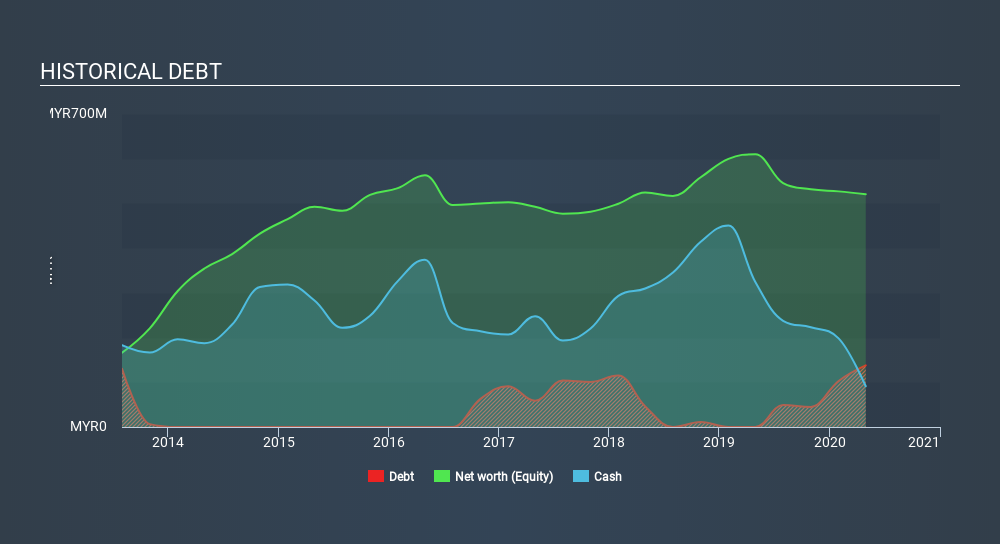

You can click the graphic below for the historical numbers, but it shows that as of April 2020 Bermaz Auto Berhad had RM137.8m of debt, an increase on none, over one year. However, it does have RM91.1m in cash offsetting this, leading to net debt of about RM46.7m.

How Strong Is Bermaz Auto Berhad's Balance Sheet?

According to the last reported balance sheet, Bermaz Auto Berhad had liabilities of RM560.8m due within 12 months, and liabilities of RM184.3m due beyond 12 months. On the other hand, it had cash of RM91.1m and RM110.3m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM543.6m.

Bermaz Auto Berhad has a market capitalization of RM1.72b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Bermaz Auto Berhad's net debt is only 0.42 times its EBITDA. And its EBIT covers its interest expense a whopping 40.3 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. It is just as well that Bermaz Auto Berhad's load is not too heavy, because its EBIT was down 60% over the last year. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Bermaz Auto Berhad can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent three years, Bermaz Auto Berhad recorded free cash flow of 48% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

We feel some trepidation about Bermaz Auto Berhad's difficulty EBIT growth rate, but we've got positives to focus on, too. For example, its interest cover and net debt to EBITDA give us some confidence in its ability to manage its debt. We think that Bermaz Auto Berhad's debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with Bermaz Auto Berhad (including 1 which is is a bit unpleasant) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

When trading Bermaz Auto Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bermaz Auto Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:BAUTO

Bermaz Auto Berhad

An investment holding company, distributes and retails of new and used Mazda, Peugeot, Kia, and XPeng vehicles in Malaysia and the Philippines.

Excellent balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor