- Malaysia

- /

- Real Estate

- /

- KLSE:EWINT

Here's Why Eco World International Berhad (KLSE:EWINT) Can Manage Its Debt Responsibly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Eco World International Berhad (KLSE:EWINT) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Eco World International Berhad

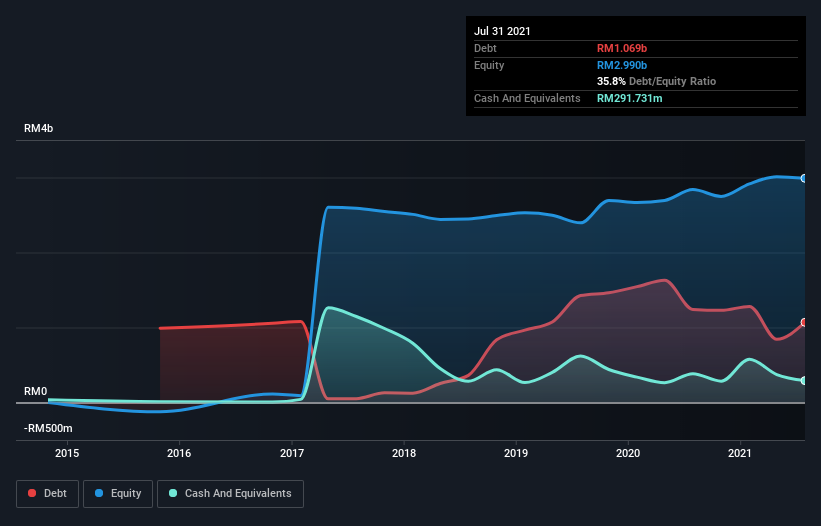

How Much Debt Does Eco World International Berhad Carry?

You can click the graphic below for the historical numbers, but it shows that Eco World International Berhad had RM1.07b of debt in July 2021, down from RM1.24b, one year before. However, because it has a cash reserve of RM291.7m, its net debt is less, at about RM777.6m.

How Healthy Is Eco World International Berhad's Balance Sheet?

We can see from the most recent balance sheet that Eco World International Berhad had liabilities of RM529.3m falling due within a year, and liabilities of RM584.4m due beyond that. On the other hand, it had cash of RM291.7m and RM10.3m worth of receivables due within a year. So its liabilities total RM811.7m more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of RM1.14b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Eco World International Berhad shareholders face the double whammy of a high net debt to EBITDA ratio (19.2), and fairly weak interest coverage, since EBIT is just 0.92 times the interest expense. This means we'd consider it to have a heavy debt load. However, it should be some comfort for shareholders to recall that Eco World International Berhad actually grew its EBIT by a hefty 239%, over the last 12 months. If that earnings trend continues it will make its debt load much more manageable in the future. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Eco World International Berhad's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Happily for any shareholders, Eco World International Berhad actually produced more free cash flow than EBIT over the last two years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

We weren't impressed with Eco World International Berhad's net debt to EBITDA, and its interest cover made us cautious. But like a ballerina ending on a perfect pirouette, it has not trouble converting EBIT to free cash flow. When we consider all the factors mentioned above, we do feel a bit cautious about Eco World International Berhad's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 5 warning signs for Eco World International Berhad you should be aware of, and 1 of them is a bit concerning.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Eco World International Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:EWINT

Eco World International Berhad

An investment holding company, engages in the property development business in the United Kingdom, Australia, and Malaysia.

Flawless balance sheet low.

Market Insights

Community Narratives