Advertisement

- Malaysia

- /

- Industrials

- /

- KLSE:TANCO

Tanco Holdings Berhad (KLSE:TANCO) Has A Pretty Healthy Balance Sheet

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Tanco Holdings Berhad (KLSE:TANCO) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Tanco Holdings Berhad

How Much Debt Does Tanco Holdings Berhad Carry?

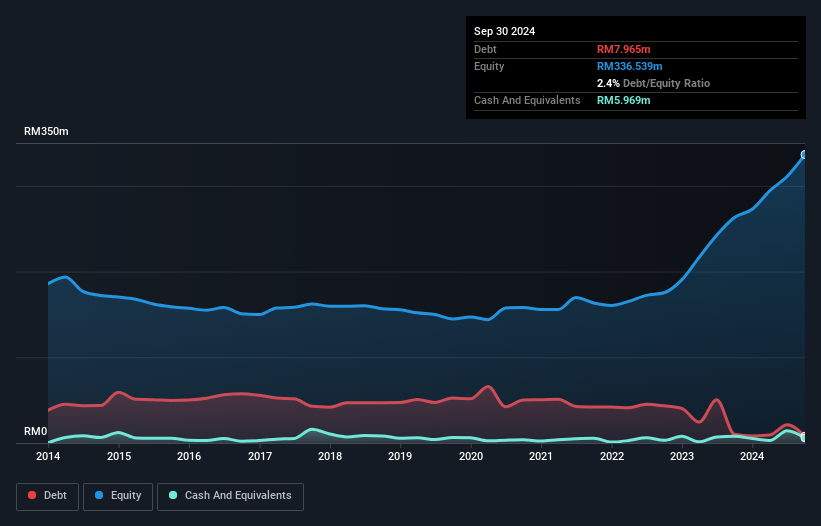

As you can see below, Tanco Holdings Berhad had RM7.97m of debt at September 2024, down from RM10.2m a year prior. However, it does have RM5.97m in cash offsetting this, leading to net debt of about RM2.00m.

A Look At Tanco Holdings Berhad's Liabilities

We can see from the most recent balance sheet that Tanco Holdings Berhad had liabilities of RM99.3m falling due within a year, and liabilities of RM40.9m due beyond that. On the other hand, it had cash of RM5.97m and RM79.5m worth of receivables due within a year. So it has liabilities totalling RM54.7m more than its cash and near-term receivables, combined.

Having regard to Tanco Holdings Berhad's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the RM4.09b company is short on cash, but still worth keeping an eye on the balance sheet. But either way, Tanco Holdings Berhad has virtually no net debt, so it's fair to say it does not have a heavy debt load!

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With debt at a measly 0.086 times EBITDA and EBIT covering interest a whopping 22.9 times, it's clear that Tanco Holdings Berhad is not a desperate borrower. Indeed relative to its earnings its debt load seems light as a feather. Fortunately, Tanco Holdings Berhad grew its EBIT by 7.2% in the last year, making that debt load look even more manageable. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Tanco Holdings Berhad can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. During the last two years, Tanco Holdings Berhad burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Based on what we've seen Tanco Holdings Berhad is not finding it easy, given its conversion of EBIT to free cash flow, but the other factors we considered give us cause to be optimistic. In particular, we are dazzled with its interest cover. Considering this range of data points, we think Tanco Holdings Berhad is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with Tanco Holdings Berhad , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Tanco Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TANCO

Tanco Holdings Berhad

An investment holding company, engages in the property development business primarily in Malaysia.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor