Advertisement

- Malaysia

- /

- Real Estate

- /

- KLSE:IWCITY

Revenues Not Telling The Story For Iskandar Waterfront City Berhad (KLSE:IWCITY) After Shares Rise 28%

Iskandar Waterfront City Berhad (KLSE:IWCITY) shares have continued their recent momentum with a 28% gain in the last month alone. The annual gain comes to 200% following the latest surge, making investors sit up and take notice.

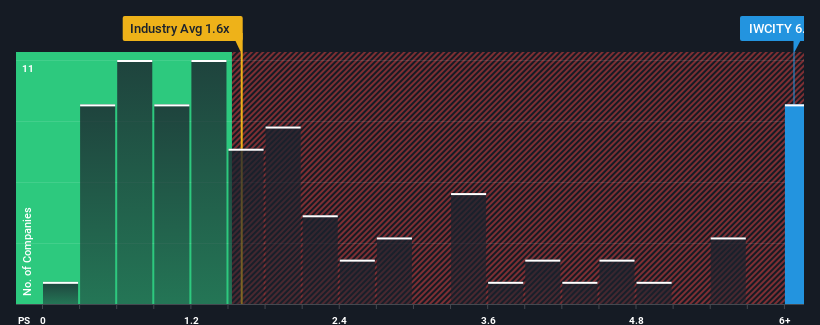

Following the firm bounce in price, given around half the companies in Malaysia's Real Estate industry have price-to-sales ratios (or "P/S") below 1.6x, you may consider Iskandar Waterfront City Berhad as a stock to avoid entirely with its 6.1x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for Iskandar Waterfront City Berhad

What Does Iskandar Waterfront City Berhad's Recent Performance Look Like?

With revenue growth that's exceedingly strong of late, Iskandar Waterfront City Berhad has been doing very well. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Iskandar Waterfront City Berhad will help you shine a light on its historical performance.How Is Iskandar Waterfront City Berhad's Revenue Growth Trending?

Iskandar Waterfront City Berhad's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Retrospectively, the last year delivered an explosive gain to the company's top line. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 3.4% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

In contrast to the company, the rest of the industry is expected to grow by 9.5% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we find it worrying that Iskandar Waterfront City Berhad's P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

What We Can Learn From Iskandar Waterfront City Berhad's P/S?

Shares in Iskandar Waterfront City Berhad have seen a strong upwards swing lately, which has really helped boost its P/S figure. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Iskandar Waterfront City Berhad revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. With a revenue decline on investors' minds, the likelihood of a souring sentiment is quite high which could send the P/S back in line with what we'd expect. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

You need to take note of risks, for example - Iskandar Waterfront City Berhad has 2 warning signs (and 1 which can't be ignored) we think you should know about.

If these risks are making you reconsider your opinion on Iskandar Waterfront City Berhad, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:IWCITY

Iskandar Waterfront City Berhad

An investment holding company, engages in the property development and construction business in Malaysia.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|3.6% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor