Advertisement

- Malaysia

- /

- Real Estate

- /

- KLSE:IWCITY

Is Iskandar Waterfront City Berhad (KLSE:IWCITY) Using Too Much Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Iskandar Waterfront City Berhad (KLSE:IWCITY) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Iskandar Waterfront City Berhad

What Is Iskandar Waterfront City Berhad's Net Debt?

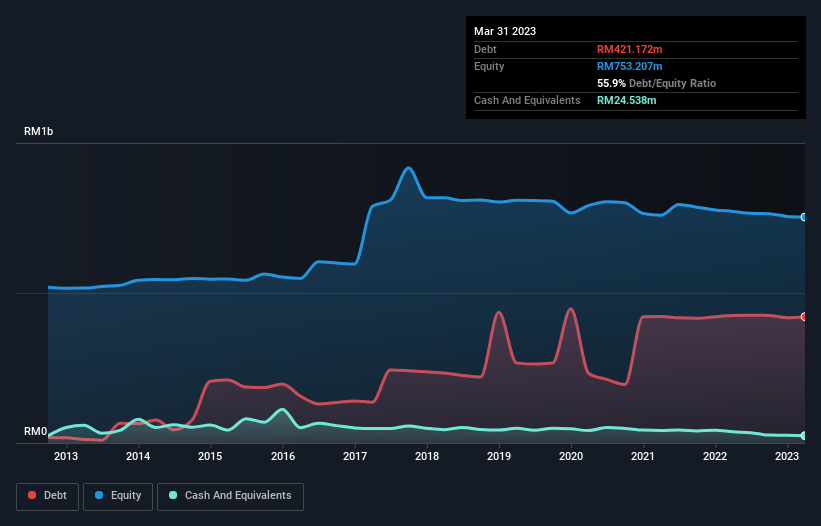

As you can see below, Iskandar Waterfront City Berhad had RM421.2m of debt, at March 2023, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of RM24.5m, its net debt is less, at about RM396.6m.

A Look At Iskandar Waterfront City Berhad's Liabilities

We can see from the most recent balance sheet that Iskandar Waterfront City Berhad had liabilities of RM289.3m falling due within a year, and liabilities of RM406.5m due beyond that. Offsetting these obligations, it had cash of RM24.5m as well as receivables valued at RM157.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM514.3m.

This deficit casts a shadow over the RM336.2m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Iskandar Waterfront City Berhad would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 0.0064 times and a disturbingly high net debt to EBITDA ratio of 792 hit our confidence in Iskandar Waterfront City Berhad like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. One redeeming factor for Iskandar Waterfront City Berhad is that it turned last year's EBIT loss into a gain of RM140k, over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Iskandar Waterfront City Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, Iskandar Waterfront City Berhad actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

On the face of it, Iskandar Waterfront City Berhad's net debt to EBITDA left us tentative about the stock, and its interest cover was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that Iskandar Waterfront City Berhad's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 3 warning signs for Iskandar Waterfront City Berhad (2 shouldn't be ignored) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:IWCITY

Iskandar Waterfront City Berhad

An investment holding company, engages in the property development and construction business in Malaysia.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor