Advertisement

Duopharma Biotech Berhad (KLSE:DPHARMA) Investors Should Think About This Before Buying It For Its Dividend

Could Duopharma Biotech Berhad (KLSE:DPHARMA) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. If you are hoping to live on the income from dividends, it's important to be a lot more stringent with your investments than the average punter.

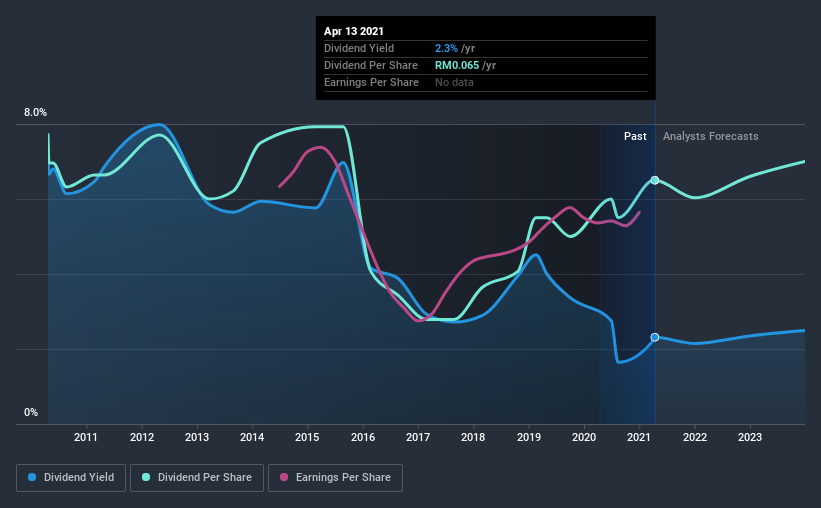

A slim 2.3% yield is hard to get excited about, but the long payment history is respectable. At the right price, or with strong growth opportunities, Duopharma Biotech Berhad could have potential. Some simple research can reduce the risk of buying Duopharma Biotech Berhad for its dividend - read on to learn more.

Click the interactive chart for our full dividend analysis

Payout ratios

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. Duopharma Biotech Berhad paid out 77% of its profit as dividends, over the trailing twelve month period. Paying out a majority of its earnings limits the amount that can be reinvested in the business. This may indicate a commitment to paying a dividend, or a dearth of investment opportunities.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. Duopharma Biotech Berhad paid out 132% of its free cash flow last year, which we think is concerning if cash flows do not improve. Paying out more than 100% of your free cash flow in dividends is generally not a long-term, sustainable state of affairs, so we think shareholders should watch this metric closely. Duopharma Biotech Berhad paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough free cash flow to cover the dividend. Cash is king, as they say, and were Duopharma Biotech Berhad to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

We update our data on Duopharma Biotech Berhad every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. For the purpose of this article, we only scrutinise the last decade of Duopharma Biotech Berhad's dividend payments. Its dividend payments have declined on at least one occasion over the past 10 years. During the past 10-year period, the first annual payment was RM0.08 in 2011, compared to RM0.07 last year. This works out to be a decline of approximately 1.7% per year over that time. Duopharma Biotech Berhad's dividend has been cut sharply at least once, so it hasn't fallen by 1.7% every year, but this is a decent approximation of the long term change.

We struggle to make a case for buying Duopharma Biotech Berhad for its dividend, given that payments have shrunk over the past 10 years.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. While there may be fluctuations in the past , Duopharma Biotech Berhad's earnings per share have basically not grown from where they were five years ago. Flat earnings per share are acceptable for a time, but over the long term, the purchasing power of the company's dividends could be eroded by inflation. Earnings are not growing quickly at all, and the company is paying out most of its profit as dividends. That's fine as far as it goes, but we're less enthusiastic as this often signals that the dividend is likely to grow slower in the future.

Conclusion

To summarise, shareholders should always check that Duopharma Biotech Berhad's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. First, the company has a payout ratio that was within an average range for most dividend stocks, but it paid out virtually all of its generated cash flow. Unfortunately, the company has not been able to generate earnings growth, and cut its dividend at least once in the past. With this information in mind, we think Duopharma Biotech Berhad may not be an ideal dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For example, we've picked out 4 warning signs for Duopharma Biotech Berhad that investors should know about before committing capital to this stock.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

When trading Duopharma Biotech Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:DPHARMA

Duopharma Biotech Berhad

An investment holding company, researches, develops, manufactures, distributes, and imports pharmaceutical products and medicines in Malaysia and internationally.

Undervalued with proven track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor