- Malaysia

- /

- Paper and Forestry Products

- /

- KLSE:WTK

Is W T K Holdings Berhad (KLSE:WTK) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that W T K Holdings Berhad (KLSE:WTK) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for W T K Holdings Berhad

What Is W T K Holdings Berhad's Debt?

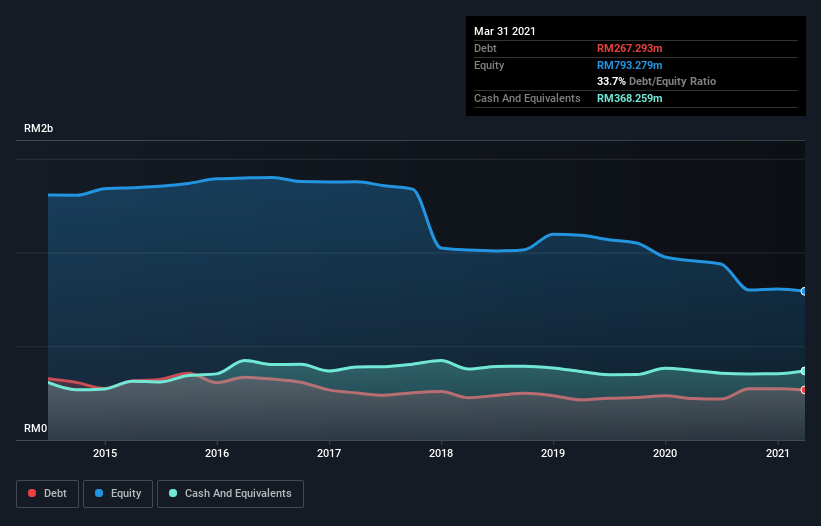

As you can see below, at the end of March 2021, W T K Holdings Berhad had RM267.3m of debt, up from RM221.3m a year ago. Click the image for more detail. But on the other hand it also has RM368.3m in cash, leading to a RM101.0m net cash position.

How Healthy Is W T K Holdings Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that W T K Holdings Berhad had liabilities of RM185.7m due within 12 months and liabilities of RM175.4m due beyond that. On the other hand, it had cash of RM368.3m and RM36.3m worth of receivables due within a year. So it actually has RM43.4m more liquid assets than total liabilities.

This surplus suggests that W T K Holdings Berhad is using debt in a way that is appears to be both safe and conservative. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Succinctly put, W T K Holdings Berhad boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is W T K Holdings Berhad's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, W T K Holdings Berhad made a loss at the EBIT level, and saw its revenue drop to RM332m, which is a fall of 36%. To be frank that doesn't bode well.

So How Risky Is W T K Holdings Berhad?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that W T K Holdings Berhad had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of RM47m and booked a RM154m accounting loss. With only RM101.0m on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 4 warning signs with W T K Holdings Berhad (at least 1 which makes us a bit uncomfortable) , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade W T K Holdings Berhad, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if W T K Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:WTK

W T K Holdings Berhad

An investment holding company, operates in the timber industry in Malaysia, Japan, Singapore, Taiwan, Australia, Thailand, and internationally.

Adequate balance sheet and slightly overvalued.

Market Insights

Community Narratives