Advertisement

- Malaysia

- /

- Basic Materials

- /

- KLSE:QUALITY

We Think Quality Concrete Holdings Berhad (KLSE:QUALITY) Can Stay On Top Of Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Quality Concrete Holdings Berhad (KLSE:QUALITY) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Quality Concrete Holdings Berhad

How Much Debt Does Quality Concrete Holdings Berhad Carry?

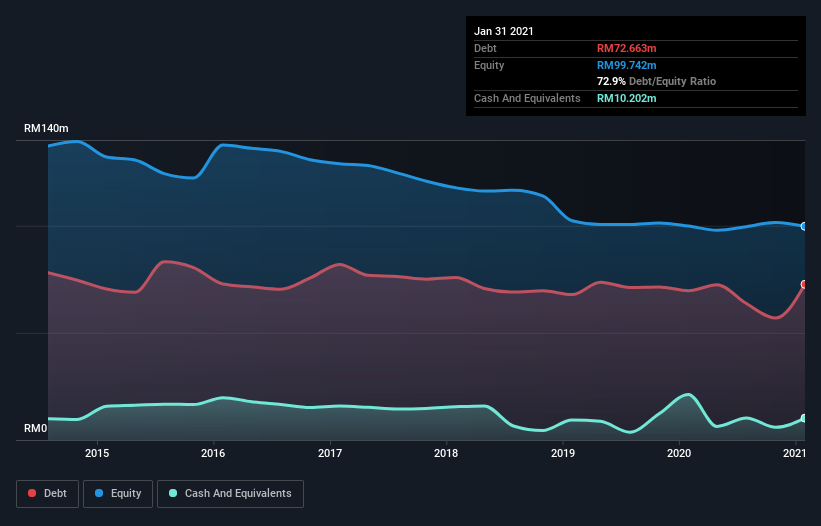

The image below, which you can click on for greater detail, shows that Quality Concrete Holdings Berhad had debt of RM63.8m at the end of January 2021, a reduction from RM69.7m over a year. However, because it has a cash reserve of RM10.2m, its net debt is less, at about RM53.6m.

How Strong Is Quality Concrete Holdings Berhad's Balance Sheet?

The latest balance sheet data shows that Quality Concrete Holdings Berhad had liabilities of RM127.9m due within a year, and liabilities of RM11.5m falling due after that. On the other hand, it had cash of RM10.2m and RM65.8m worth of receivables due within a year. So it has liabilities totalling RM63.4m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of RM82.9m, so it does suggest shareholders should keep an eye on Quality Concrete Holdings Berhad's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While we wouldn't worry about Quality Concrete Holdings Berhad's net debt to EBITDA ratio of 3.8, we think its super-low interest cover of 1.7 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. However, it should be some comfort for shareholders to recall that Quality Concrete Holdings Berhad actually grew its EBIT by a hefty 210%, over the last 12 months. If it can keep walking that path it will be in a position to shed its debt with relative ease. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Quality Concrete Holdings Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Quality Concrete Holdings Berhad actually produced more free cash flow than EBIT over the last two years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Quality Concrete Holdings Berhad's conversion of EBIT to free cash flow was a real positive on this analysis, as was its EBIT growth rate. But truth be told its interest cover had us nibbling our nails. Considering this range of data points, we think Quality Concrete Holdings Berhad is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Quality Concrete Holdings Berhad has 3 warning signs (and 2 which are significant) we think you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Quality Concrete Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:QUALITY

Quality Concrete Holdings Berhad

An investment holding company, manufactures, trades, and sells ready-mixed concrete and concrete products in Malaysia.

Slight risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor