Advertisement

Is Nylex (Malaysia) Berhad (KLSE:NYLEX) Using Too Much Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Nylex (Malaysia) Berhad (KLSE:NYLEX) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Nylex (Malaysia) Berhad

What Is Nylex (Malaysia) Berhad's Net Debt?

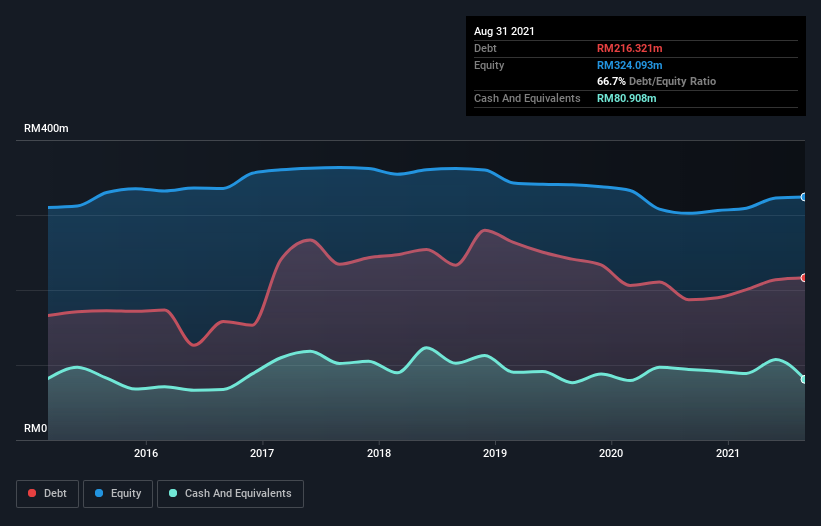

As you can see below, at the end of August 2021, Nylex (Malaysia) Berhad had RM216.3m of debt, up from RM187.0m a year ago. Click the image for more detail. On the flip side, it has RM80.9m in cash leading to net debt of about RM135.4m.

How Healthy Is Nylex (Malaysia) Berhad's Balance Sheet?

According to the last reported balance sheet, Nylex (Malaysia) Berhad had liabilities of RM322.9m due within 12 months, and liabilities of RM50.6m due beyond 12 months. Offsetting these obligations, it had cash of RM80.9m as well as receivables valued at RM213.7m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM78.8m.

Nylex (Malaysia) Berhad has a market capitalization of RM236.7m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Nylex (Malaysia) Berhad's debt is 3.3 times its EBITDA, and its EBIT cover its interest expense 5.6 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Notably, Nylex (Malaysia) Berhad made a loss at the EBIT level, last year, but improved that to positive EBIT of RM31m in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Nylex (Malaysia) Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, Nylex (Malaysia) Berhad saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

We'd go so far as to say Nylex (Malaysia) Berhad's conversion of EBIT to free cash flow was disappointing. But at least its interest cover is not so bad. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Nylex (Malaysia) Berhad stock a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 4 warning signs for Nylex (Malaysia) Berhad (2 are concerning) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Nylex (Malaysia) Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:NYLEX

Nylex (Malaysia) Berhad

Nylex (Malaysia) Berhad, an investment holding company, manufactures and markets vinyl-coated fabrics in Malaysia.

Flawless balance sheet with weak fundamentals.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.7% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor