Advertisement

- Malaysia

- /

- Metals and Mining

- /

- KLSE:HIAPTEK

Hiap Teck Venture Berhad (KLSE:HIAPTEK) Shares May Have Slumped 28% But Getting In Cheap Is Still Unlikely

Hiap Teck Venture Berhad (KLSE:HIAPTEK) shares have had a horrible month, losing 28% after a relatively good period beforehand. Longer-term shareholders would now have taken a real hit with the stock declining 2.8% in the last year.

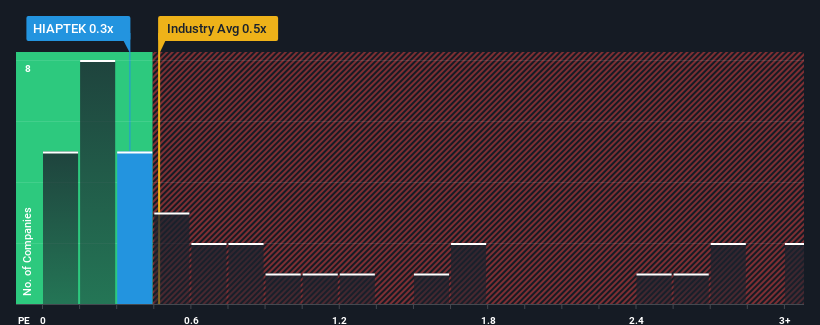

Although its price has dipped substantially, there still wouldn't be many who think Hiap Teck Venture Berhad's price-to-sales (or "P/S") ratio of 0.3x is worth a mention when the median P/S in Malaysia's Metals and Mining industry is similar at about 0.5x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Hiap Teck Venture Berhad

How Has Hiap Teck Venture Berhad Performed Recently?

Hiap Teck Venture Berhad certainly has been doing a good job lately as its revenue growth has been positive while most other companies have been seeing their revenue go backwards. It might be that many expect the strong revenue performance to deteriorate like the rest, which has kept the P/S ratio from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Want the full picture on analyst estimates for the company? Then our free report on Hiap Teck Venture Berhad will help you uncover what's on the horizon.How Is Hiap Teck Venture Berhad's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Hiap Teck Venture Berhad's is when the company's growth is tracking the industry closely.

Taking a look back first, we see that the company managed to grow revenues by a handy 13% last year. This was backed up an excellent period prior to see revenue up by 53% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue growth is heading into negative territory, declining 3.6% over the next year. Meanwhile, the broader industry is forecast to expand by 9.2%, which paints a poor picture.

In light of this, it's somewhat alarming that Hiap Teck Venture Berhad's P/S sits in line with the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh on the share price eventually.

The Final Word

Hiap Teck Venture Berhad's plummeting stock price has brought its P/S back to a similar region as the rest of the industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

It appears that Hiap Teck Venture Berhad currently trades on a higher than expected P/S for a company whose revenues are forecast to decline. With this in mind, we don't feel the current P/S is justified as declining revenues are unlikely to support a more positive sentiment for long. If the poor revenue outlook tells us one thing, it's that these current price levels could be unsustainable.

Before you settle on your opinion, we've discovered 1 warning sign for Hiap Teck Venture Berhad that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Hiap Teck Venture Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KLSE:HIAPTEK

Hiap Teck Venture Berhad

Manufactures, rents, distributes, and sells steel pipes, hollow sections, scaffolding equipment and accessories, and other steel products in Malaysia.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor