Advertisement

- Malaysia

- /

- Paper and Forestry Products

- /

- KLSE:HEXRTL

How Much Is Classic Scenic Berhad (KLSE:CSCENIC) Paying Its CEO?

Samuel Lim became the CEO of Classic Scenic Berhad (KLSE:CSCENIC) in 2004, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether Classic Scenic Berhad pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

Check out our latest analysis for Classic Scenic Berhad

Comparing Classic Scenic Berhad's CEO Compensation With the industry

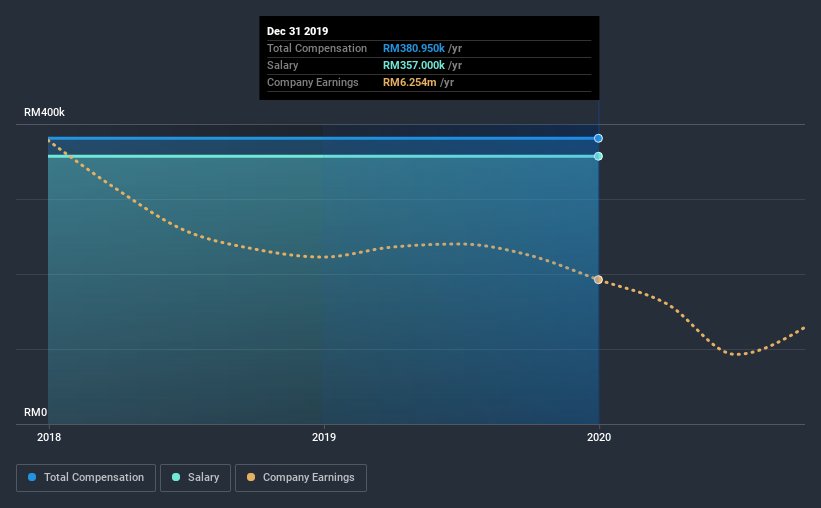

Our data indicates that Classic Scenic Berhad has a market capitalization of RM110m, and total annual CEO compensation was reported as RM381k for the year to December 2019. That's mostly flat as compared to the prior year's compensation. We note that the salary portion, which stands at RM357.0k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the industry with market capitalizations below RM812m, we found that the median total CEO compensation was RM526k. This suggests that Classic Scenic Berhad remunerates its CEO largely in line with the industry average.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | RM357k | RM357k | 94% |

| Other | RM24k | RM24k | 6% |

| Total Compensation | RM381k | RM381k | 100% |

On an industry level, roughly 89% of total compensation represents salary and 11% is other remuneration. Classic Scenic Berhad is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Classic Scenic Berhad's Growth

Classic Scenic Berhad has reduced its earnings per share by 30% a year over the last three years. In the last year, its revenue is down 26%.

Few shareholders would be pleased to read that EPS have declined. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Classic Scenic Berhad Been A Good Investment?

With a three year total loss of 34% for the shareholders, Classic Scenic Berhad would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be lessto generous with CEO compensation.

In Summary...

As we noted earlier, Classic Scenic Berhad pays its CEO in line with similar-sized companies belonging to the same industry. In the meantime, the company has reported declining EPS growth and shareholder returns over the last three years. Considering overall performance, shareholders will likely hold off support for a raise until results improve.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We did our research and identified 4 warning signs (and 1 which shouldn't be ignored) in Classic Scenic Berhad we think you should know about.

Important note: Classic Scenic Berhad is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you’re looking to trade Classic Scenic Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hextar Retail Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:HEXRTL

Hextar Retail Berhad

An investment holding company, engages in the manufacture and sale of wooden picture frame moldings in North America, Australia, Malaysia, and internationally.

Flawless balance sheet with questionable track record.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1341 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative