Advertisement

Is Box-Pak (Malaysia) Bhd (KLSE:BOXPAK) Using Debt In A Risky Way?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Box-Pak (Malaysia) Bhd. (KLSE:BOXPAK) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Box-Pak (Malaysia) Bhd

How Much Debt Does Box-Pak (Malaysia) Bhd Carry?

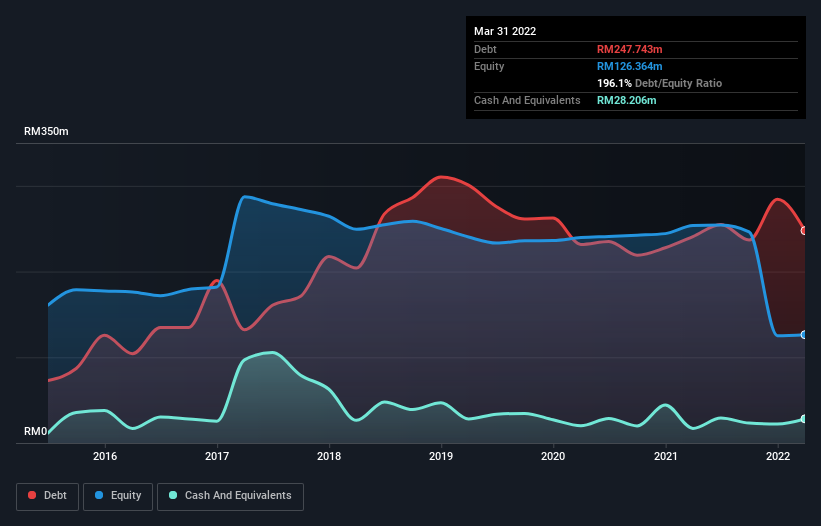

The chart below, which you can click on for greater detail, shows that Box-Pak (Malaysia) Bhd had RM247.7m in debt in March 2022; about the same as the year before. However, it does have RM28.2m in cash offsetting this, leading to net debt of about RM219.5m.

A Look At Box-Pak (Malaysia) Bhd's Liabilities

The latest balance sheet data shows that Box-Pak (Malaysia) Bhd had liabilities of RM412.4m due within a year, and liabilities of RM50.2m falling due after that. On the other hand, it had cash of RM28.2m and RM199.4m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM235.1m.

This deficit casts a shadow over the RM150.1m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Box-Pak (Malaysia) Bhd would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But it is Box-Pak (Malaysia) Bhd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Box-Pak (Malaysia) Bhd's revenue was pretty flat, and it made a negative EBIT. While that's not too bad, we'd prefer see growth.

Caveat Emptor

Importantly, Box-Pak (Malaysia) Bhd had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping RM22m. When we look at that alongside the significant liabilities, we're not particularly confident about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it had negative free cash flow of RM26m over the last twelve months. So suffice it to say we consider the stock to be risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with Box-Pak (Malaysia) Bhd (at least 2 which shouldn't be ignored) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Box-Pak (Malaysia) Bhd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:BOXPAK

Box-Pak (Malaysia) Bhd

An investment holding company, engages in the manufacture and distribution of paper boxes, cartons, general papers, and board printing products in Malaysia, Vietnam, and Myanmar.

Good value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|6.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|25.8% undervalued

KA

Community Contributor