Advertisement

- Malaysia

- /

- Electronic Equipment and Components

- /

- KLSE:ARTRONIQ

Slowing Rates Of Return At Artroniq Berhad (KLSE:ARTRONIQ) Leave Little Room For Excitement

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. In light of that, when we looked at Artroniq Berhad (KLSE:ARTRONIQ) and its ROCE trend, we weren't exactly thrilled.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Artroniq Berhad:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

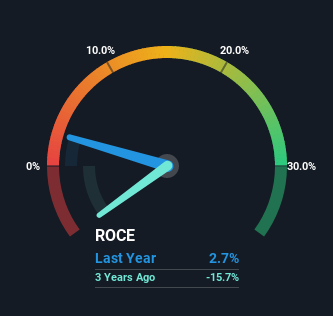

0.027 = RM1.4m ÷ (RM64m - RM15m) (Based on the trailing twelve months to March 2022).

Thus, Artroniq Berhad has an ROCE of 2.7%. In absolute terms, that's a low return and it also under-performs the Chemicals industry average of 8.7%.

View our latest analysis for Artroniq Berhad

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Artroniq Berhad, check out these free graphs here.

How Are Returns Trending?

There are better returns on capital out there than what we're seeing at Artroniq Berhad. The company has employed 42% more capital in the last five years, and the returns on that capital have remained stable at 2.7%. Given the company has increased the amount of capital employed, it appears the investments that have been made simply don't provide a high return on capital.

The Bottom Line On Artroniq Berhad's ROCE

In summary, Artroniq Berhad has simply been reinvesting capital and generating the same low rate of return as before. Investors must think there's better things to come because the stock has knocked it out of the park, delivering a 106% gain to shareholders who have held over the last five years. Ultimately, if the underlying trends persist, we wouldn't hold our breath on it being a multi-bagger going forward.

Artroniq Berhad does have some risks though, and we've spotted 3 warning signs for Artroniq Berhad that you might be interested in.

While Artroniq Berhad isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:ARTRONIQ

Artroniq Berhad

An investment holding company, provides trading of information and communication technology (ICT) products and related services, management services, and semiconductor in Malaysia, Asia, the Middle East, the United States, and internationally.

Mediocre balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets