Advertisement

Are Ancom Berhad's (KLSE:ANCOM) Statutory Earnings A Good Reflection Of Its Earnings Potential?

It might be old fashioned, but we really like to invest in companies that make a profit, each and every year. That said, the current statutory profit is not always a good guide to a company's underlying profitability. In this article, we'll look at how useful this year's statutory profit is, when analysing Ancom Berhad (KLSE:ANCOM).

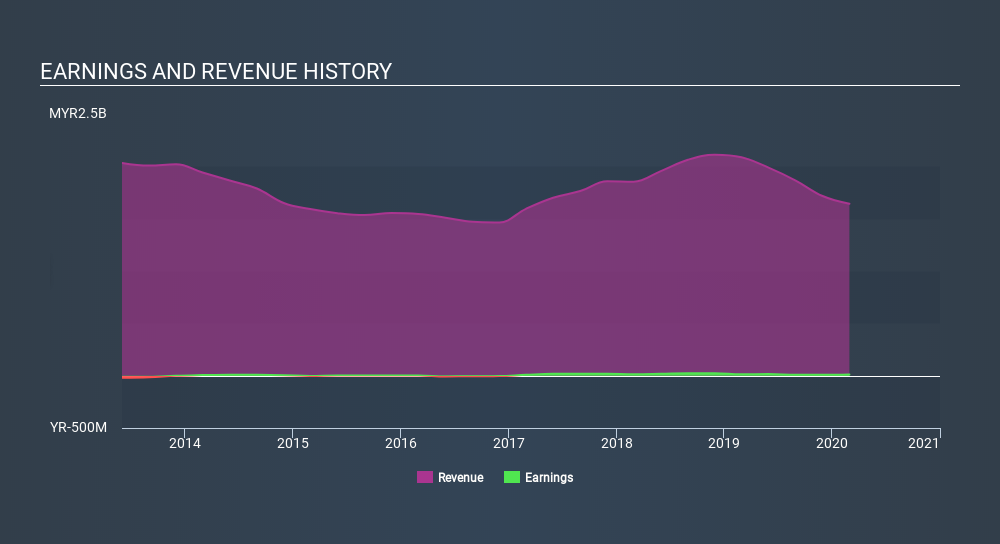

It's good to see that over the last twelve months Ancom Berhad made a profit of RM12.3m on revenue of RM1.64b. One positive is that it has grown both its profit and its revenue, over the last few years, though not in the last twelve months.

Check out our latest analysis for Ancom Berhad

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. So today we'll look at what Ancom Berhad's cashflow tells us about the quality of its earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Ancom Berhad.

Zooming In On Ancom Berhad's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

For the year to February 2020, Ancom Berhad had an accrual ratio of -0.10. That indicates that its free cash flow was a fair bit more than its statutory profit. In fact, it had free cash flow of RM83m in the last year, which was a lot more than its statutory profit of RM12.3m. Ancom Berhad shareholders are no doubt pleased that free cash flow improved over the last twelve months.

Our Take On Ancom Berhad's Profit Performance

As we discussed above, Ancom Berhad has perfectly satisfactory free cash flow relative to profit. Because of this, we think Ancom Berhad's earnings potential is at least as good as it seems, and maybe even better! And the EPS is up 46% annually, over the last three years. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. If you want to do dive deeper into Ancom Berhad, you'd also look into what risks it is currently facing. For example, Ancom Berhad has 3 warning signs (and 1 which is a bit concerning) we think you should know about.

This note has only looked at a single factor that sheds light on the nature of Ancom Berhad's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About KLSE:ANCOMNY

Ancom Nylex Berhad

Engages in the agricultural and industrial chemicals, public health and hygiene, animal health, polymer, logistics, information technology (IT), and media businesses in Malaysia and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.9% undervalued

TO

Community Contributor