- Malaysia

- /

- Household Products

- /

- KLSE:HEXCARE

If You Like EPS Growth Then Check Out Rubberex Corporation (M) Berhad (KLSE:RUBEREX) Before It's Too Late

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.'

So if you're like me, you might be more interested in profitable, growing companies, like Rubberex Corporation (M) Berhad (KLSE:RUBEREX). Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. Loss-making companies are always racing against time to reach financial sustainability, but time is often a friend of the profitable company, especially if it is growing.

Check out our latest analysis for Rubberex Corporation (M) Berhad

Rubberex Corporation (M) Berhad's Improving Profits

In a capitalist society capital chases profits, and that means share prices tend rise with earnings per share (EPS). So like the hint of a smile on a face that I love, growing EPS generally makes me look twice. It is therefore awe-striking that Rubberex Corporation (M) Berhad's EPS went from RM0.015 to RM0.16 in just one year. When you see earnings grow that quickly, it often means good things ahead for the company. But the key is discerning whether something profound has changed, or if this is a just a one-off boost.

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). The good news is that Rubberex Corporation (M) Berhad is growing revenues, and EBIT margins improved by 29.9 percentage points to 40%, over the last year. That's great to see, on both counts.

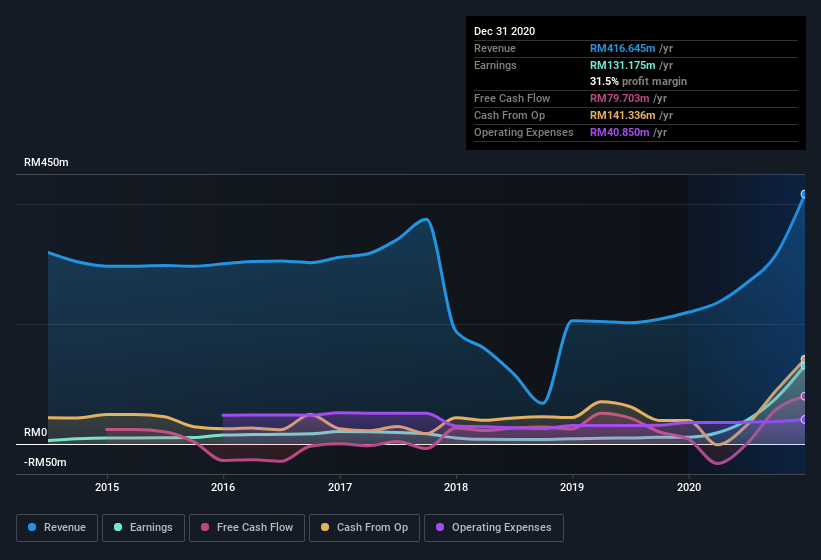

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

Since Rubberex Corporation (M) Berhad is no giant, with a market capitalization of RM982m, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Rubberex Corporation (M) Berhad Insiders Aligned With All Shareholders?

It makes me feel more secure owning shares in a company if insiders also own shares, thusly more closely aligning our interests. So it is good to see that Rubberex Corporation (M) Berhad insiders have a significant amount of capital invested in the stock. To be specific, they have RM109m worth of shares. That shows significant buy-in, and may indicate conviction in the business strategy. That amounts to 11% of the company, demonstrating a degree of high-level alignment with shareholders.

Does Rubberex Corporation (M) Berhad Deserve A Spot On Your Watchlist?

Rubberex Corporation (M) Berhad's earnings per share have taken off like a rocket aimed right at the moon. That EPS growth certainly has my attention, and the large insider ownership only serves to further stoke my interest. At times fast EPS growth is a sign the business has reached an inflection point; and I do like those. So to my mind Rubberex Corporation (M) Berhad is worth putting on your watchlist; after all, shareholders do well when the market underestimates fast growing companies. However, before you get too excited we've discovered 4 warning signs for Rubberex Corporation (M) Berhad (2 are a bit unpleasant!) that you should be aware of.

Although Rubberex Corporation (M) Berhad certainly looks good to me, I would like it more if insiders were buying up shares. If you like to see insider buying, too, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hextar Healthcare Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:HEXCARE

Hextar Healthcare Berhad

An investment holding company, produces, sells, and exports household gloves, industrial gloves, and nitrile disposable gloves in Europe, Asia, North and South America, and internationally.

Adequate balance sheet and slightly overvalued.

Market Insights

Community Narratives