Advertisement

Sime Darby Plantation Berhad's (KLSE:SIMEPLT) Stock Has Shown Weakness Lately But Financial Prospects Look Decent: Is The Market Wrong?

It is hard to get excited after looking at Sime Darby Plantation Berhad's (KLSE:SIMEPLT) recent performance, when its stock has declined 13% over the past three months. But if you pay close attention, you might find that its key financial indicators look quite decent, which could mean that the stock could potentially rise in the long-term given how markets usually reward more resilient long-term fundamentals. Particularly, we will be paying attention to Sime Darby Plantation Berhad's ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Sime Darby Plantation Berhad

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Sime Darby Plantation Berhad is:

9.7% = RM1.6b ÷ RM16b (Based on the trailing twelve months to March 2021).

The 'return' is the amount earned after tax over the last twelve months. That means that for every MYR1 worth of shareholders' equity, the company generated MYR0.10 in profit.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Sime Darby Plantation Berhad's Earnings Growth And 9.7% ROE

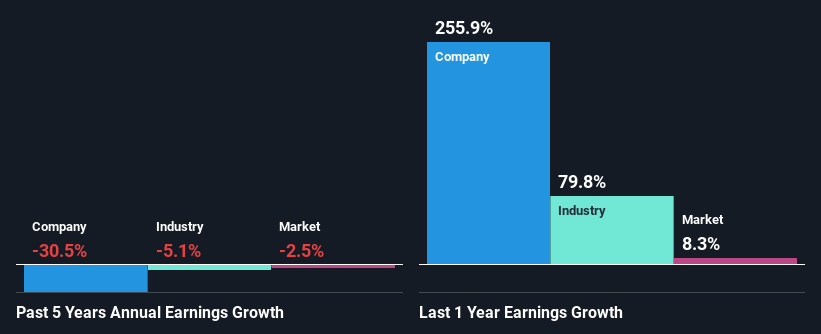

On the face of it, Sime Darby Plantation Berhad's ROE is not much to talk about. However, the fact that the company's ROE is higher than the average industry ROE of 7.6%, is definitely interesting. However, Sime Darby Plantation Berhad's five year net income decline rate was 31%. Bear in mind, the company does have a slightly low ROE. It is just that the industry ROE is lower. So that could be one of the factors that are causing earnings growth to shrink.

Next, when we compared with the industry, which has shrunk its earnings at a rate of 5.1% in the same period, we still found Sime Darby Plantation Berhad's performance to be quite bleak, because the company has been shrinking its earnings faster than the industry.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. Is SIMEPLT fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is Sime Darby Plantation Berhad Using Its Retained Earnings Effectively?

Looking at its three-year median payout ratio of 37% (or a retention ratio of 63%) which is pretty normal, Sime Darby Plantation Berhad's declining earnings is rather baffling as one would expect to see a fair bit of growth when a company is retaining a good portion of its profits. So there could be some other explanations in that regard. For instance, the company's business may be deteriorating.

Moreover, Sime Darby Plantation Berhad has been paying dividends for three years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer consistent dividends even though earnings have been shrinking. Our latest analyst data shows that the future payout ratio of the company is expected to rise to 61% over the next three years. Despite the higher expected payout ratio, the company's ROE is not expected to change by much.

Summary

Overall, we feel that Sime Darby Plantation Berhad certainly does have some positive factors to consider. Although, we are disappointed to see a lack of growth in earnings even in spite of a moderate ROE and and a high reinvestment rate. We believe that there might be some outside factors that could be having a negative impact on the business. Having said that, we studied the latest analyst forecasts, and found that analysts are expecting the company's earnings growth to improve slightly. Sure enough, this could bring some relief to shareholders. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:SDG

SD Guthrie Berhad

Operates as an integrated plantations company in Malaysia and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor