Be Wary Of Sime Darby Plantation Berhad (KLSE:SIMEPLT) And Its Returns On Capital

When it comes to investing, there are some useful financial metrics that can warn us when a business is potentially in trouble. Businesses in decline often have two underlying trends, firstly, a declining return on capital employed (ROCE) and a declining base of capital employed. This combination can tell you that not only is the company investing less, it's earning less on what it does invest. In light of that, from a first glance at Sime Darby Plantation Berhad (KLSE:SIMEPLT), we've spotted some signs that it could be struggling, so let's investigate.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Sime Darby Plantation Berhad, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

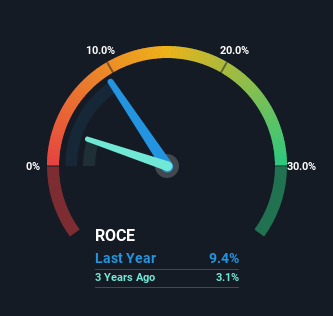

0.094 = RM2.4b ÷ (RM32b - RM5.9b) (Based on the trailing twelve months to March 2023).

Thus, Sime Darby Plantation Berhad has an ROCE of 9.4%. On its own that's a low return on capital but it's in line with the industry's average returns of 8.5%.

View our latest analysis for Sime Darby Plantation Berhad

Above you can see how the current ROCE for Sime Darby Plantation Berhad compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Sime Darby Plantation Berhad.

How Are Returns Trending?

We are a bit worried about the trend of returns on capital at Sime Darby Plantation Berhad. About five years ago, returns on capital were 12%, however they're now substantially lower than that as we saw above. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Since returns are falling and the business has the same amount of assets employed, this can suggest it's a mature business that hasn't had much growth in the last five years. If these trends continue, we wouldn't expect Sime Darby Plantation Berhad to turn into a multi-bagger.

In Conclusion...

In summary, it's unfortunate that Sime Darby Plantation Berhad is generating lower returns from the same amount of capital. And, the stock has remained flat over the last five years, so investors don't seem too impressed either. Unless there is a shift to a more positive trajectory in these metrics, we would look elsewhere.

One more thing: We've identified 2 warning signs with Sime Darby Plantation Berhad (at least 1 which is a bit unpleasant) , and understanding these would certainly be useful.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SDG

SD Guthrie Berhad

An investment holding company, operates as an integrated plantations company in Malaysia and internationally.

Flawless balance sheet unattractive dividend payer.