Advertisement

What Do The Returns At Riverview Rubber Estates Berhad (KLSE:RVIEW) Mean Going Forward?

What are the early trends we should look for to identify a stock that could multiply in value over the long term? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So on that note, Riverview Rubber Estates Berhad (KLSE:RVIEW) looks quite promising in regards to its trends of return on capital.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Riverview Rubber Estates Berhad is:

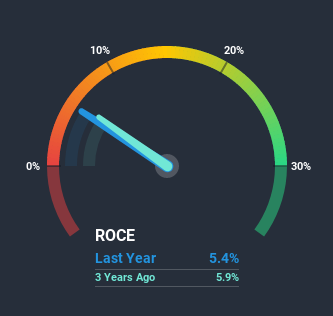

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.054 = RM16m ÷ (RM315m - RM11m) (Based on the trailing twelve months to December 2020).

Thus, Riverview Rubber Estates Berhad has an ROCE of 5.4%. Ultimately, that's a low return and it under-performs the Food industry average of 7.7%.

View our latest analysis for Riverview Rubber Estates Berhad

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Riverview Rubber Estates Berhad's past further, check out this free graph of past earnings, revenue and cash flow.

The Trend Of ROCE

Riverview Rubber Estates Berhad is showing promise given that its ROCE is trending up and to the right. The figures show that over the last five years, ROCE has grown 88% whilst employing roughly the same amount of capital. So it's likely that the business is now reaping the full benefits of its past investments, since the capital employed hasn't changed considerably. It's worth looking deeper into this though because while it's great that the business is more efficient, it might also mean that going forward the areas to invest internally for the organic growth are lacking.

The Bottom Line On Riverview Rubber Estates Berhad's ROCE

As discussed above, Riverview Rubber Estates Berhad appears to be getting more proficient at generating returns since capital employed has remained flat but earnings (before interest and tax) are up. Astute investors may have an opportunity here because the stock has declined 16% in the last five years. With that in mind, we believe the promising trends warrant this stock for further investigation.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 2 warning signs for Riverview Rubber Estates Berhad (of which 1 can't be ignored!) that you should know about.

While Riverview Rubber Estates Berhad isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you’re looking to trade Riverview Rubber Estates Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:RVIEW

Riverview Rubber Estates Berhad

Engages in the cultivation of oil palm in Peninsular Malaysia.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.6% undervalued

MA

Community Contributor