Advertisement

Shareholders Should Be Pleased With Nestlé (Malaysia) Berhad's (KLSE:NESTLE) Price

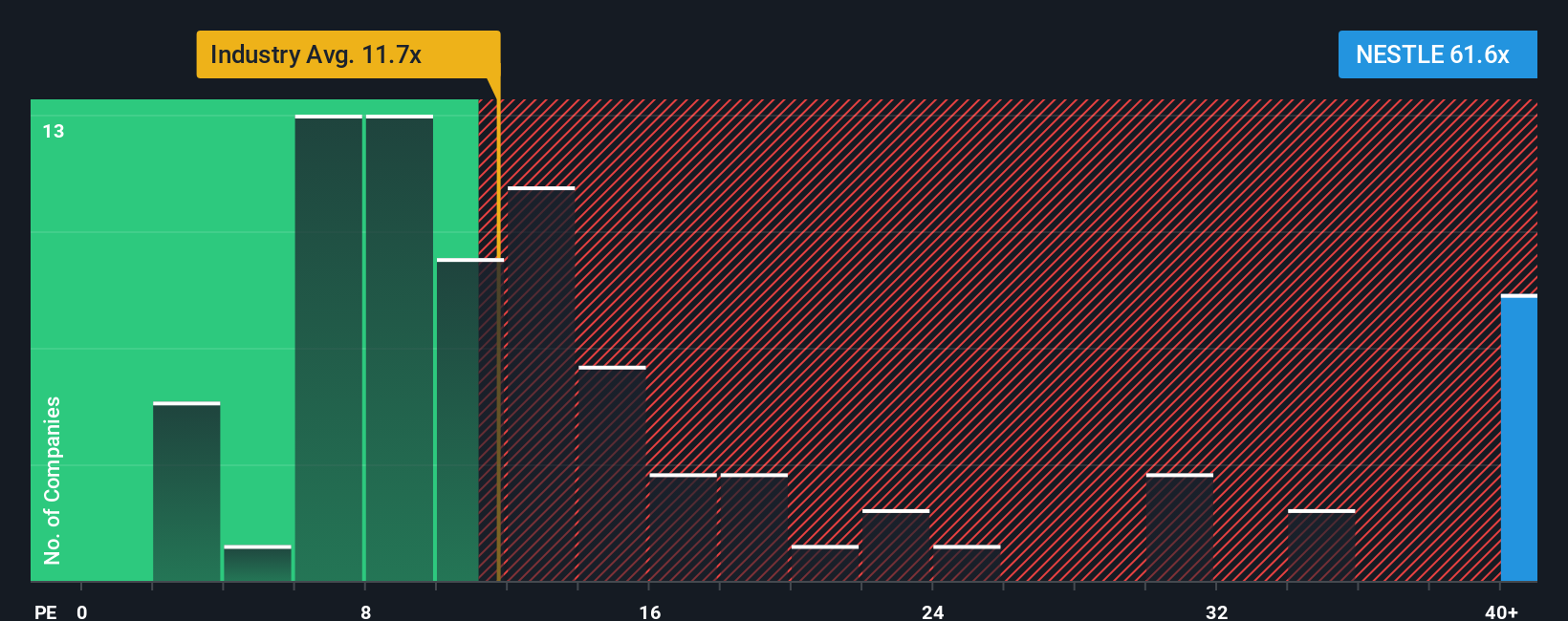

With a price-to-earnings (or "P/E") ratio of 61.6x Nestlé (Malaysia) Berhad (KLSE:NESTLE) may be sending very bearish signals at the moment, given that almost half of all companies in Malaysia have P/E ratios under 14x and even P/E's lower than 9x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

While the market has experienced earnings growth lately, Nestlé (Malaysia) Berhad's earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Nestlé (Malaysia) Berhad

How Is Nestlé (Malaysia) Berhad's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as Nestlé (Malaysia) Berhad's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 30% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 37% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 15% per annum over the next three years. With the market only predicted to deliver 12% per year, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Nestlé (Malaysia) Berhad's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Nestlé (Malaysia) Berhad's P/E?

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Nestlé (Malaysia) Berhad's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

It is also worth noting that we have found 1 warning sign for Nestlé (Malaysia) Berhad that you need to take into consideration.

You might be able to find a better investment than Nestlé (Malaysia) Berhad. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Nestlé (Malaysia) Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:NESTLE

Nestlé (Malaysia) Berhad

Manufactures and sells food and beverage products in Malaysia and internationally.

Moderate growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets