Kim Loong Resources Berhad (KLSE:KMLOONG) Is Increasing Its Dividend To RM0.05

Kim Loong Resources Berhad's (KLSE:KMLOONG) dividend will be increasing to RM0.05 on 29th of August. This will take the dividend yield from 7.3% to 7.3%, providing a nice boost to shareholder returns.

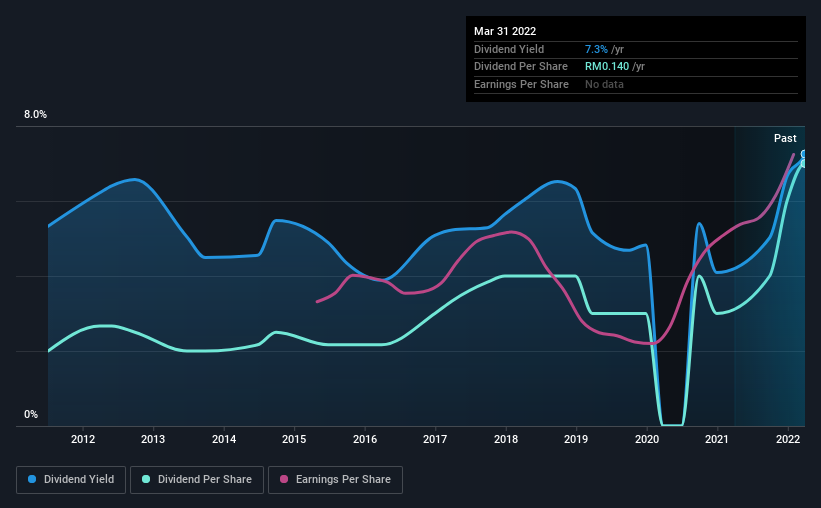

See our latest analysis for Kim Loong Resources Berhad

Kim Loong Resources Berhad's Earnings Easily Cover the Distributions

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, Kim Loong Resources Berhad's dividend was only 55% of earnings, however it was paying out 107% of free cash flows. While the company may be more focused on returning cash to shareholders than growing the business at this time, we think that a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

EPS is set to grow by 36.1% over the next year. If recent patterns in the dividend continues, the payout ratio in 12 months could be 77% which is a bit high but can definitely be sustainable.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2012, the dividend has gone from RM0.04 to RM0.14. This means that it has been growing its distributions at 13% per annum over that time. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. It's encouraging to see Kim Loong Resources Berhad has been growing its earnings per share at 13% a year over the past five years. While on an earnings basis, this company looks appealing as an income stock, the cash payout ratio still makes us cautious.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Kim Loong Resources Berhad's payments are rock solid. While Kim Loong Resources Berhad is earning enough to cover the payments, the cash flows are lacking. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Just as an example, we've come across 3 warning signs for Kim Loong Resources Berhad you should be aware of, and 1 of them is concerning. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Kim Loong Resources Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KMLOONG

Kim Loong Resources Berhad

An investment holding company, engages in the cultivation of oil palm in Malaysia.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion