Advertisement

Shareholders May Not Be So Generous With Khee San Berhad's (KLSE:KHEESAN) CEO Compensation And Here's Why

Key Insights

- Khee San Berhad to hold its Annual General Meeting on 28th of November

- Total pay for CEO Edward Tan includes RM480.0k salary

- The overall pay is 95% above the industry average

- Khee San Berhad's EPS grew by 121% over the past three years while total shareholder return over the past three years was 108%

CEO Edward Tan has done a decent job of delivering relatively good performance at Khee San Berhad (KLSE:KHEESAN) recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 28th of November. However, some shareholders will still be cautious of paying the CEO excessively.

View our latest analysis for Khee San Berhad

Comparing Khee San Berhad's CEO Compensation With The Industry

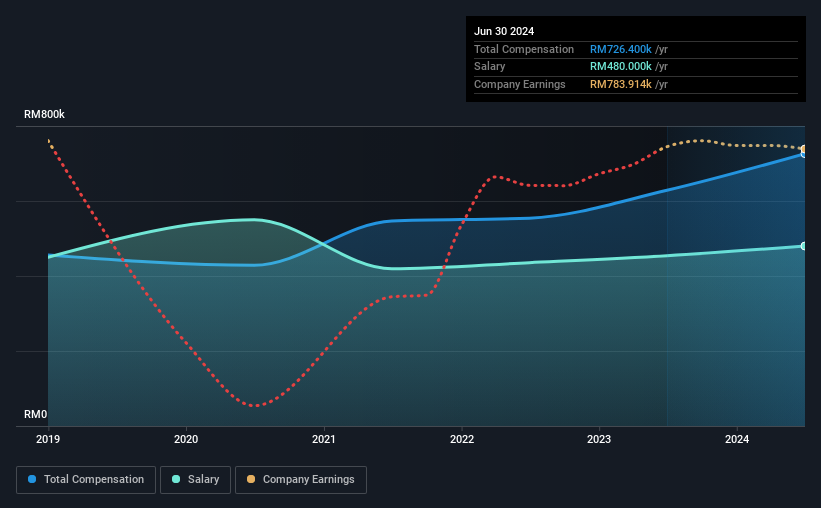

Our data indicates that Khee San Berhad has a market capitalization of RM34m, and total annual CEO compensation was reported as RM726k for the year to June 2024. That's a notable increase of 16% on last year. We note that the salary portion, which stands at RM480.0k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the Malaysian Food industry with market capitalizations below RM893m, we found that the median total CEO compensation was RM373k. Hence, we can conclude that Edward Tan is remunerated higher than the industry median.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | RM480k | RM454k | 66% |

| Other | RM246k | RM175k | 34% |

| Total Compensation | RM726k | RM629k | 100% |

On an industry level, roughly 62% of total compensation represents salary and 38% is other remuneration. Our data reveals that Khee San Berhad allocates salary more or less in line with the wider market. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Khee San Berhad's Growth

Over the past three years, Khee San Berhad has seen its earnings per share (EPS) grow by 121% per year. In the last year, its revenue is down 5.9%.

Shareholders would be glad to know that the company has improved itself over the last few years. It's always a tough situation when revenues are not growing, but ultimately profits are more important. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Khee San Berhad Been A Good Investment?

Most shareholders would probably be pleased with Khee San Berhad for providing a total return of 108% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We did our research and identified 6 warning signs (and 3 which are a bit unpleasant) in Khee San Berhad we think you should know about.

Switching gears from Khee San Berhad, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Khee San Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KHEESAN

Khee San Berhad

An investment holding company, manufactures and distributes candies confectionery and wafer products in Malaysia, Europe, Africa, and Rest of Asia.

Slight and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor