Advertisement

Earnings Not Telling The Story For Hap Seng Plantations Holdings Berhad (KLSE:HSPLANT) After Shares Rise 29%

Hap Seng Plantations Holdings Berhad (KLSE:HSPLANT) shareholders have had their patience rewarded with a 29% share price jump in the last month. Looking back a bit further, it's encouraging to see the stock is up 26% in the last year.

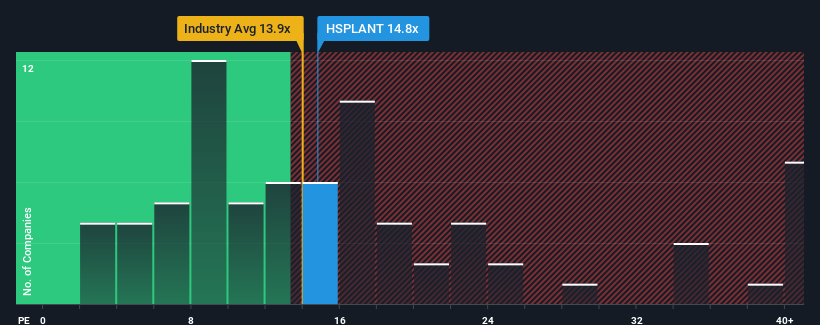

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Hap Seng Plantations Holdings Berhad's P/E ratio of 14.8x, since the median price-to-earnings (or "P/E") ratio in Malaysia is also close to 16x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

With earnings growth that's superior to most other companies of late, Hap Seng Plantations Holdings Berhad has been doing relatively well. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

View our latest analysis for Hap Seng Plantations Holdings Berhad

Does Growth Match The P/E?

In order to justify its P/E ratio, Hap Seng Plantations Holdings Berhad would need to produce growth that's similar to the market.

If we review the last year of earnings growth, the company posted a terrific increase of 65%. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 12% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Shifting to the future, estimates from the nine analysts covering the company suggest earnings growth is heading into negative territory, declining 3.8% each year over the next three years. That's not great when the rest of the market is expected to grow by 14% each year.

In light of this, it's somewhat alarming that Hap Seng Plantations Holdings Berhad's P/E sits in line with the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the negative growth outlook.

The Key Takeaway

Hap Seng Plantations Holdings Berhad's stock has a lot of momentum behind it lately, which has brought its P/E level with the market. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Hap Seng Plantations Holdings Berhad's analyst forecasts revealed that its outlook for shrinking earnings isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings are unlikely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Plus, you should also learn about these 2 warning signs we've spotted with Hap Seng Plantations Holdings Berhad (including 1 which is potentially serious).

If you're unsure about the strength of Hap Seng Plantations Holdings Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Hap Seng Plantations Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:HSPLANT

Hap Seng Plantations Holdings Berhad

An investment holding company, operates as an oil palm plantation company in Malaysia.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|37.6% undervalued

TR

Community Contributor