Advertisement

Is CCK Consolidated Holdings Berhad (KLSE:CCK) A Risky Investment?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that CCK Consolidated Holdings Berhad (KLSE:CCK) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for CCK Consolidated Holdings Berhad

What Is CCK Consolidated Holdings Berhad's Net Debt?

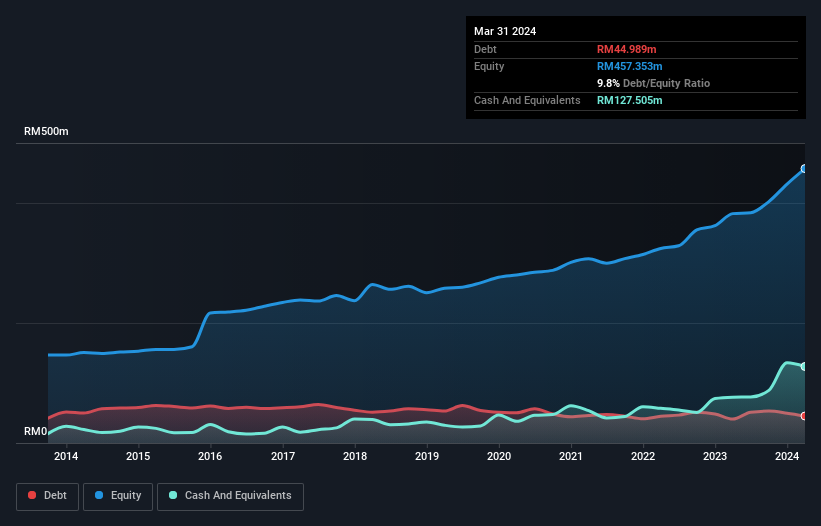

As you can see below, at the end of March 2024, CCK Consolidated Holdings Berhad had RM45.0m of debt, up from RM39.9m a year ago. Click the image for more detail. But on the other hand it also has RM127.5m in cash, leading to a RM82.5m net cash position.

How Strong Is CCK Consolidated Holdings Berhad's Balance Sheet?

According to the last reported balance sheet, CCK Consolidated Holdings Berhad had liabilities of RM106.9m due within 12 months, and liabilities of RM29.3m due beyond 12 months. Offsetting these obligations, it had cash of RM127.5m as well as receivables valued at RM81.8m due within 12 months. So it can boast RM73.1m more liquid assets than total liabilities.

This short term liquidity is a sign that CCK Consolidated Holdings Berhad could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that CCK Consolidated Holdings Berhad has more cash than debt is arguably a good indication that it can manage its debt safely.

On top of that, CCK Consolidated Holdings Berhad grew its EBIT by 64% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine CCK Consolidated Holdings Berhad's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While CCK Consolidated Holdings Berhad has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, CCK Consolidated Holdings Berhad recorded free cash flow worth 71% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While it is always sensible to investigate a company's debt, in this case CCK Consolidated Holdings Berhad has RM82.5m in net cash and a decent-looking balance sheet. And we liked the look of last year's 64% year-on-year EBIT growth. So is CCK Consolidated Holdings Berhad's debt a risk? It doesn't seem so to us. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 1 warning sign for CCK Consolidated Holdings Berhad you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KLSE:CCK

CCK Consolidated Holdings Berhad

An investment holding company, engages in the rearing and production of poultry products, prawns, and seafood products.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor