- Malaysia

- /

- Capital Markets

- /

- KLSE:KENANGA

Kenanga Investment Bank Berhad's (KLSE:KENANGA) Share Price Is Matching Sentiment Around Its Earnings

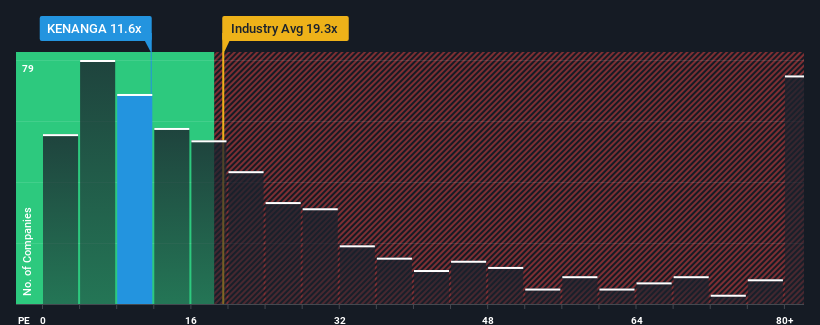

With a price-to-earnings (or "P/E") ratio of 11.6x Kenanga Investment Bank Berhad (KLSE:KENANGA) may be sending bullish signals at the moment, given that almost half of all companies in Malaysia have P/E ratios greater than 16x and even P/E's higher than 29x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

For example, consider that Kenanga Investment Bank Berhad's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the disappointing earnings performance to continue or accelerate, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Kenanga Investment Bank Berhad

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, Kenanga Investment Bank Berhad would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a frustrating 11% decrease to the company's bottom line. As a result, earnings from three years ago have also fallen 13% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 15% shows it's an unpleasant look.

With this information, we are not surprised that Kenanga Investment Bank Berhad is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. Even just maintaining these prices could be difficult to achieve as recent earnings trends are already weighing down the shares.

What We Can Learn From Kenanga Investment Bank Berhad's P/E?

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Kenanga Investment Bank Berhad maintains its low P/E on the weakness of its sliding earnings over the medium-term, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

You always need to take note of risks, for example - Kenanga Investment Bank Berhad has 2 warning signs we think you should be aware of.

If you're unsure about the strength of Kenanga Investment Bank Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Kenanga Investment Bank Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KENANGA

Kenanga Investment Bank Berhad

Provides investment banking, stockbroking, and related financial services primarily in Malaysia.

Proven track record average dividend payer.

Market Insights

Community Narratives