- Malaysia

- /

- Hospitality

- /

- KLSE:BORNOIL

We Think Borneo Oil Berhad (KLSE:BORNOIL) Can Stay On Top Of Its Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Borneo Oil Berhad (KLSE:BORNOIL) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Borneo Oil Berhad

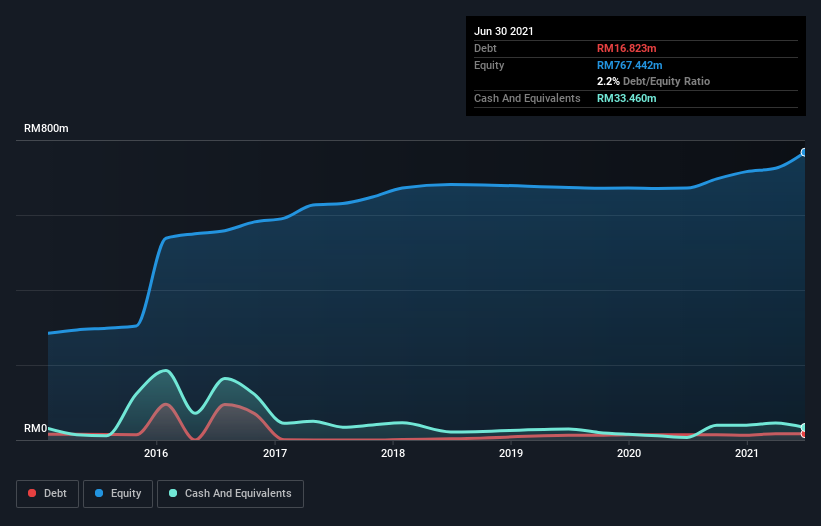

What Is Borneo Oil Berhad's Debt?

As you can see below, at the end of June 2021, Borneo Oil Berhad had RM16.8m of debt, up from RM14.1m a year ago. Click the image for more detail. But on the other hand it also has RM33.5m in cash, leading to a RM16.6m net cash position.

How Strong Is Borneo Oil Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Borneo Oil Berhad had liabilities of RM18.9m due within 12 months and liabilities of RM36.9m due beyond that. Offsetting this, it had RM33.5m in cash and RM15.5m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM6.90m.

Of course, Borneo Oil Berhad has a market capitalization of RM181.0m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Borneo Oil Berhad boasts net cash, so it's fair to say it does not have a heavy debt load!

Even more impressive was the fact that Borneo Oil Berhad grew its EBIT by 484% over twelve months. That boost will make it even easier to pay down debt going forward. When analysing debt levels, the balance sheet is the obvious place to start. But it is Borneo Oil Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Borneo Oil Berhad has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Borneo Oil Berhad saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing up

We could understand if investors are concerned about Borneo Oil Berhad's liabilities, but we can be reassured by the fact it has has net cash of RM16.6m. And we liked the look of last year's 484% year-on-year EBIT growth. So we don't have any problem with Borneo Oil Berhad's use of debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 4 warning signs for Borneo Oil Berhad (1 can't be ignored) you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Borneo Oil Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:BORNOIL

Borneo Oil Berhad

An investment holding company, operates and franchises fast food restaurants in Malaysia and Australia.

Low with imperfect balance sheet.

Market Insights

Community Narratives