Advertisement

- Malaysia

- /

- Commercial Services

- /

- KLSE:KJTS

After Leaping 25% KJTS Group Berhad (KLSE:KJTS) Shares Are Not Flying Under The Radar

Despite an already strong run, KJTS Group Berhad (KLSE:KJTS) shares have been powering on, with a gain of 25% in the last thirty days. The annual gain comes to 106% following the latest surge, making investors sit up and take notice.

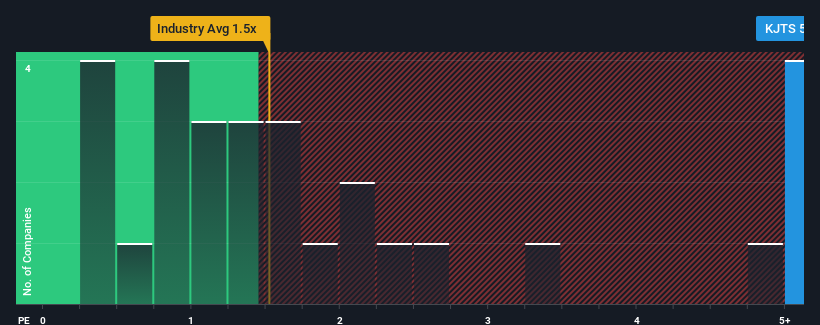

After such a large jump in price, you could be forgiven for thinking KJTS Group Berhad is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 5.7x, considering almost half the companies in Malaysia's Commercial Services industry have P/S ratios below 1.5x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for KJTS Group Berhad

How Has KJTS Group Berhad Performed Recently?

Recent times have been advantageous for KJTS Group Berhad as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on KJTS Group Berhad will help you uncover what's on the horizon.How Is KJTS Group Berhad's Revenue Growth Trending?

In order to justify its P/S ratio, KJTS Group Berhad would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered a decent 15% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 53% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 144% during the coming year according to the lone analyst following the company. That's shaping up to be materially higher than the 40% growth forecast for the broader industry.

With this information, we can see why KJTS Group Berhad is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On KJTS Group Berhad's P/S

Shares in KJTS Group Berhad have seen a strong upwards swing lately, which has really helped boost its P/S figure. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that KJTS Group Berhad maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Commercial Services industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Before you settle on your opinion, we've discovered 1 warning sign for KJTS Group Berhad that you should be aware of.

If you're unsure about the strength of KJTS Group Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if KJTS Group Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KJTS

KJTS Group Berhad

Provides integrated building support in Malaysia, Singapore, and Thailand.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor