Advertisement

- Malaysia

- /

- Commercial Services

- /

- KLSE:CABNET

Is Cabnet Holdings Berhad (KLSE:CABNET) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Cabnet Holdings Berhad (KLSE:CABNET) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Cabnet Holdings Berhad

What Is Cabnet Holdings Berhad's Debt?

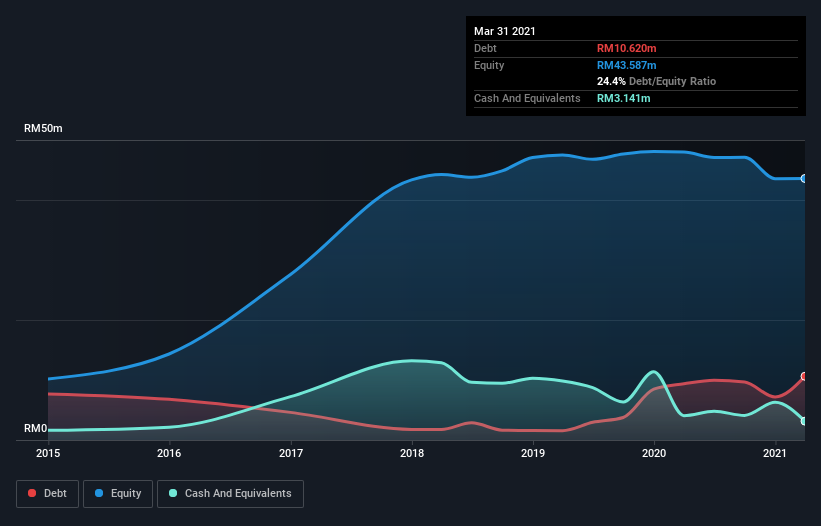

The image below, which you can click on for greater detail, shows that at March 2021 Cabnet Holdings Berhad had debt of RM10.6m, up from RM9.38m in one year. On the flip side, it has RM3.14m in cash leading to net debt of about RM7.48m.

How Healthy Is Cabnet Holdings Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Cabnet Holdings Berhad had liabilities of RM18.1m due within 12 months and liabilities of RM5.48m due beyond that. On the other hand, it had cash of RM3.14m and RM41.4m worth of receivables due within a year. So it can boast RM21.0m more liquid assets than total liabilities.

This surplus liquidity suggests that Cabnet Holdings Berhad's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. Having regard to this fact, we think its balance sheet is as strong as an ox. There's no doubt that we learn most about debt from the balance sheet. But it is Cabnet Holdings Berhad's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Cabnet Holdings Berhad made a loss at the EBIT level, and saw its revenue drop to RM44m, which is a fall of 35%. That makes us nervous, to say the least.

Caveat Emptor

Not only did Cabnet Holdings Berhad's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). To be specific the EBIT loss came in at RM4.3m. On a more positive note, the company does have liquid assets, so it has a bit of time to improve its operations before the debt becomes an acute problem. But we'd be more likely to spend time trying to understand the stock if the company made a profit. This one is a bit too risky for our liking. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Cabnet Holdings Berhad has 2 warning signs (and 1 which is a bit concerning) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:CABNET

Cabnet Holdings Berhad

An investment holding company, provides building construction and management solutions in Malaysia.

Adequate balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor