- Malaysia

- /

- Construction

- /

- KLSE:PTARAS

Pintaras Jaya Berhad (KLSE:PTARAS) Will Pay A Larger Dividend Than Last Year At MYR0.05

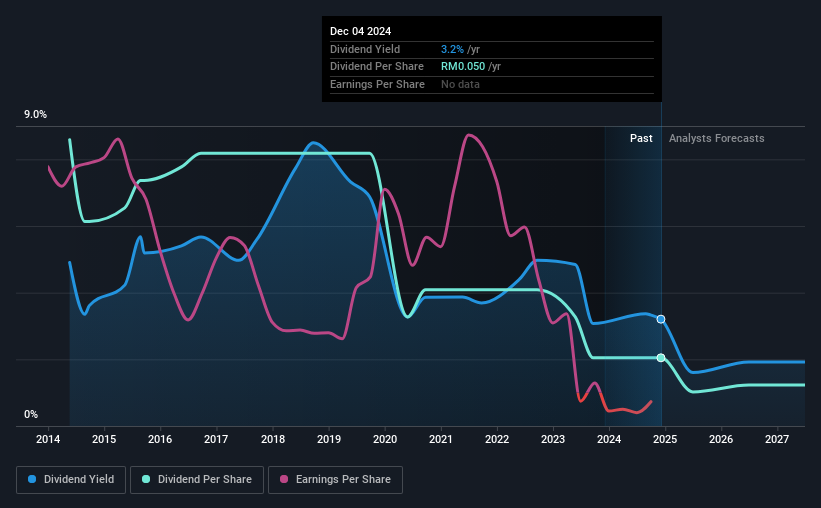

Pintaras Jaya Berhad (KLSE:PTARAS) has announced that it will be increasing its dividend from last year's comparable payment on the 15th of January to MYR0.05. This will take the dividend yield to an attractive 3.2%, providing a nice boost to shareholder returns.

View our latest analysis for Pintaras Jaya Berhad

Pintaras Jaya Berhad's Projections Indicate Future Payments May Be Unsustainable

Estimates Indicate Pintaras Jaya Berhad's Could Struggle to Maintain Dividend Payments In The Future

Pintaras Jaya Berhad's Future Dividends May Potentially Be At Risk

A big dividend yield for a few years doesn't mean much if it can't be sustained. Pintaras Jaya Berhad is unprofitable despite paying a dividend, and it is paying out 102% of its free cash flow. This makes us feel that the dividend will be hard to maintain.

Over the next year, EPS is forecast to grow rapidly. Assuming the dividend continues along recent trends, we could see the payout ratio reach 120%, which is on the unsustainable side.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The dividend has gone from an annual total of MYR0.21 in 2014 to the most recent total annual payment of MYR0.05. Dividend payments have fallen sharply, down 76% over that time. A company that decreases its dividend over time generally isn't what we are looking for.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS is growing. Pintaras Jaya Berhad's EPS has fallen by approximately 39% per year during the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

Pintaras Jaya Berhad's Dividend Doesn't Look Great

Overall, while the dividend being raised can be good, there are some concerns about its long term sustainability. The company isn't making enough to be paying as much as it is, and the other factors don't look particularly promising either. Overall, this doesn't get us very excited from an income standpoint.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 2 warning signs for Pintaras Jaya Berhad (of which 1 is a bit unpleasant!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:PTARAS

Pintaras Jaya Berhad

An investment holding company, engages in undertaking piling contracts, civil engineering, and building construction works in Malaysia and Singapore.

Excellent balance sheet with reasonable growth potential.