Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:PLB

Here's Why PLB Engineering Berhad (KLSE:PLB) Is Weighed Down By Its Debt Load

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, PLB Engineering Berhad (KLSE:PLB) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View 6 warning signs we detected for PLB Engineering Berhad

What Is PLB Engineering Berhad's Debt?

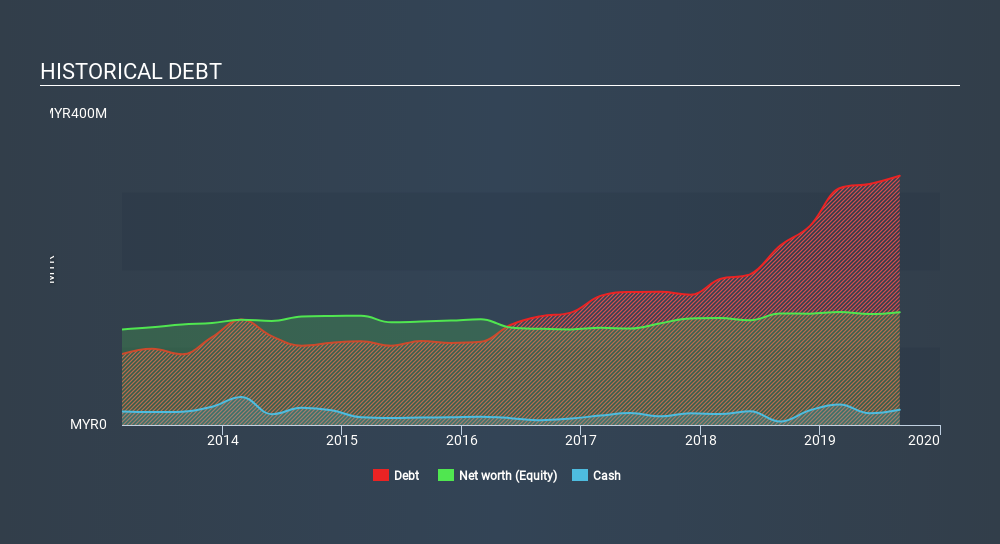

You can click the graphic below for the historical numbers, but it shows that as of August 2019 PLB Engineering Berhad had RM320.5m of debt, an increase on RM231, over one year. On the flip side, it has RM19.6m in cash leading to net debt of about RM300.9m.

How Healthy Is PLB Engineering Berhad's Balance Sheet?

We can see from the most recent balance sheet that PLB Engineering Berhad had liabilities of RM199.5m falling due within a year, and liabilities of RM221.4m due beyond that. On the other hand, it had cash of RM19.6m and RM112.7m worth of receivables due within a year. So it has liabilities totalling RM288.7m more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the RM175.3m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, PLB Engineering Berhad would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 2.3 times and a disturbingly high net debt to EBITDA ratio of 10.1 hit our confidence in PLB Engineering Berhad like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. The silver lining is that PLB Engineering Berhad grew its EBIT by 218% last year, which nourishing like the idealism of youth. If it can keep walking that path it will be in a position to shed its debt with relative ease. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 6 warning signs for PLB Engineering Berhad (of which 4 are major) which any shareholder or potential investor should be aware of.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, PLB Engineering Berhad burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both PLB Engineering Berhad's conversion of EBIT to free cash flow and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least it's pretty decent at growing its EBIT; that's encouraging. Overall, it seems to us that PLB Engineering Berhad's balance sheet is really quite a risk to the business. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. Over time, share prices tend to follow earnings per share, so if you're interested in PLB Engineering Berhad, you may well want to click here to check an interactive graph of its earnings per share history.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About KLSE:PLB

PLB Engineering Berhad

An investment holding company, engages in the contracting and construction of industrial, residential, and commercial building and renovation works in Malaysia.

Low risk and overvalued.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|65.7% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.9% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.4% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.0% undervalued

AN

Based on Analyst Price Targets