- Malaysia

- /

- Trade Distributors

- /

- KLSE:KPS

These 4 Measures Indicate That Kumpulan Perangsang Selangor Berhad (KLSE:KPS) Is Using Debt Extensively

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Kumpulan Perangsang Selangor Berhad (KLSE:KPS) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Kumpulan Perangsang Selangor Berhad

What Is Kumpulan Perangsang Selangor Berhad's Net Debt?

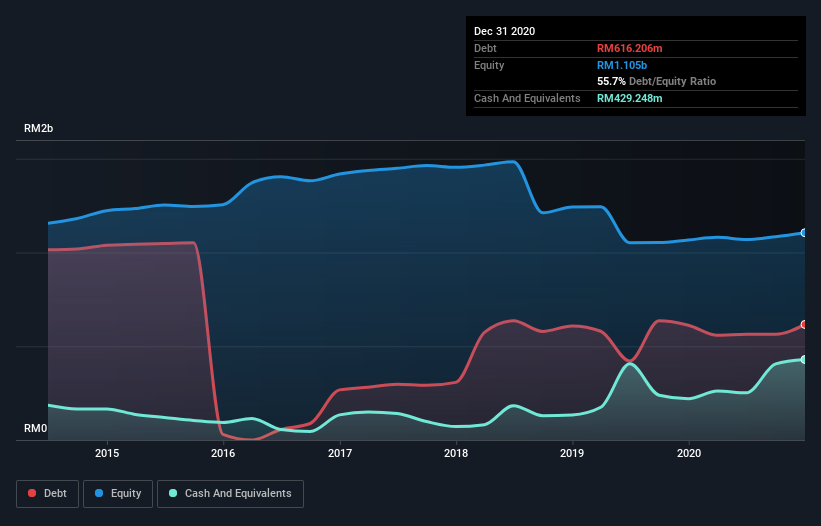

The chart below, which you can click on for greater detail, shows that Kumpulan Perangsang Selangor Berhad had RM616.2m in debt in December 2020; about the same as the year before. However, because it has a cash reserve of RM429.2m, its net debt is less, at about RM187.0m.

How Strong Is Kumpulan Perangsang Selangor Berhad's Balance Sheet?

According to the last reported balance sheet, Kumpulan Perangsang Selangor Berhad had liabilities of RM471.1m due within 12 months, and liabilities of RM699.9m due beyond 12 months. Offsetting these obligations, it had cash of RM429.2m as well as receivables valued at RM415.6m due within 12 months. So it has liabilities totalling RM326.1m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Kumpulan Perangsang Selangor Berhad has a market capitalization of RM548.1m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Even though Kumpulan Perangsang Selangor Berhad's debt is only 2.3, its interest cover is really very low at 1.6. In large part that's it has so much depreciation and amortisation. These charges may be non-cash, so they could be excluded when it comes to paying down debt. But the accounting charges are there for a reason -- some assets are seen to be losing value. Either way there's no doubt the stock is using meaningful leverage. Shareholders should be aware that Kumpulan Perangsang Selangor Berhad's EBIT was down 30% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Kumpulan Perangsang Selangor Berhad's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Kumpulan Perangsang Selangor Berhad created free cash flow amounting to 16% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

On the face of it, Kumpulan Perangsang Selangor Berhad's interest cover left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability handle its debt, based on its EBITDA, isn't such a worry. Overall, it seems to us that Kumpulan Perangsang Selangor Berhad's balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with Kumpulan Perangsang Selangor Berhad (including 2 which are significant) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kumpulan Perangsang Selangor Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:KPS

Kumpulan Perangsang Selangor Berhad

An investment holding company, engages in manufacturing, trading, licensing, infrastructure, oil and gas, and property investment businesses.

Excellent balance sheet with proven track record and pays a dividend.

Market Insights

Community Narratives