- Malaysia

- /

- Trade Distributors

- /

- KLSE:KNUSFOR

Here's Why Knusford Berhad (KLSE:KNUSFOR) Has A Meaningful Debt Burden

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Knusford Berhad (KLSE:KNUSFOR) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Knusford Berhad

How Much Debt Does Knusford Berhad Carry?

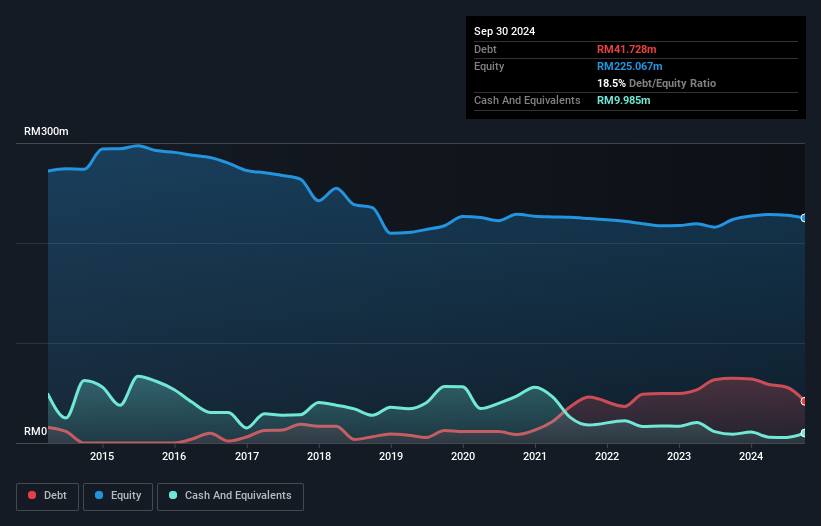

You can click the graphic below for the historical numbers, but it shows that Knusford Berhad had RM41.7m of debt in September 2024, down from RM64.6m, one year before. However, it does have RM9.99m in cash offsetting this, leading to net debt of about RM31.7m.

A Look At Knusford Berhad's Liabilities

According to the last reported balance sheet, Knusford Berhad had liabilities of RM172.9m due within 12 months, and liabilities of RM1.06m due beyond 12 months. Offsetting these obligations, it had cash of RM9.99m as well as receivables valued at RM222.1m due within 12 months. So it actually has RM58.2m more liquid assets than total liabilities.

This surplus strongly suggests that Knusford Berhad has a rock-solid balance sheet (and the debt is of no concern whatsoever). With this in mind one could posit that its balance sheet means the company is able to handle some adversity.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Knusford Berhad has a debt to EBITDA ratio of 2.5 and its EBIT covered its interest expense 2.6 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Unfortunately, Knusford Berhad's EBIT flopped 16% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Knusford Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last two years, Knusford Berhad saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Neither Knusford Berhad's ability to convert EBIT to free cash flow nor its EBIT growth rate gave us confidence in its ability to take on more debt. But its level of total liabilities tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that Knusford Berhad is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example Knusford Berhad has 3 warning signs (and 1 which is a bit concerning) we think you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Knusford Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KNUSFOR

Knusford Berhad

An investment holding company, provides machinery, equipment, reconditioning workshop and transportation services in Malaysia.

Adequate balance sheet low.

Market Insights

Community Narratives